This secret indicator is genius. And it’s trying to give you a warning

When it comes to forecasting long-term stock returns, more than a dozen models are competing for the title of ‘world’s greatest predictor’. But one obscure choice is head and shoulders above the rest, writes Stéphane Renevier.

29th December 2023 08:32

by Stéphane Renevier from Finimize

- When investors allocate too much to stocks, stocks subsequently go down. When they allocate too little, stocks subsequently go up.

- And right now, investors are holding an extreme amount of stocks, suggesting that future returns will be very poor – and even negative.

- To protect yourself, you could underweight stocks until investors’ average allocation to stocks drops below 40%.

When it comes to forecasting long-term stock returns, more than a dozen models are competing for the title of “world’s greatest predictor”. But one obscure choice is head and shoulders above the rest – and right now, its message isn't exactly brimming with optimism.

What’s this little-known indicator?

The idea – conceived by the anonymous author of this 2013 blog post – is simple: when investors on aggregate allocate too much of their capital to stocks, stocks subsequently underperform. The reverse is true too: when investors shun stocks for other investments, stocks subsequently outperform.

In fact, simply looking at investors’ average stock allocation would’ve historically helped us predict – incredibly accurately – whether subsequent 10-year returns would be high or low. Every time investors have allocated more than 40% to stocks, they have experienced losses over the following decade. The higher the allocation, the lower the subsequent returns.

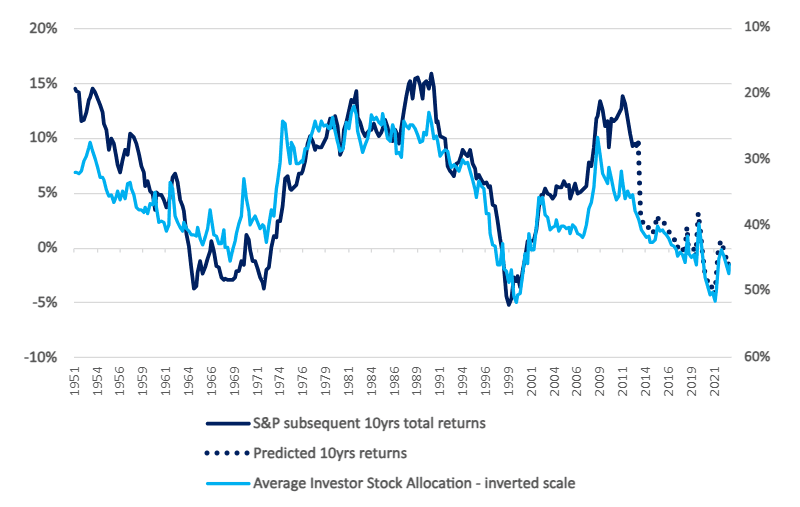

The indicator suggests that stocks’ returns aren’t likely to be positive over the next decade. Source: Philosophical Economics blog, Fred data, Finimize. Past performance is not a guide to future performance.

How can you tell how much investors are allocating to stocks?

Investors’ average allocation to stocks is simply the market value of all stocks over the total value of all financial assets (which includes stocks, cash, and all types of bonds). It’s not actually as easy to work out as it seems, but fortunately, you don’t need to: the creator of this indicator kindly does it for you here.

What you do need to know is how to calculate the numerator of that equation: the market value of all stocks is the total number of shares multiplied by the price of those shares. Put simply, it’s the total market capitalisation of every stock in the world. Meanwhile, the denominator - the total value of all financial assets – doesn’t just include the market value of stocks, but also the total amount of liabilities of all borrowers (i.e. cash and bonds).

Howdoes this indicator predict stock market returns?

To make sense of that, we need to look at the calculation above more closely:

Investors’ average allocation to stocks = market value of stocks / (market value of stocks + total value of liabilities of all borrowers)

If the total liabilities of all borrowers grows with the economy – a realistic assumption given that businesses finance a big part of their expansion through loans or bonds – then the market value of stocks must also grow. Investors, after all, want to keep their allocation to stocks steady. And if the denominator increases, the numerator needs to as well in order for the ratio to remain constant.

So if the target stock allocation is constant, the market value of stockshas to increase. And there are two ways that can happen: either companies issue new shares, or the price of all stocks – i.e. the stock market – goes up.

And that’s where it gets interesting: the corporate sector realistically can’t issue enough shares each year to keep up with the increasing supply of cash and bonds, so stock priceshave torise over the long term if investors want to keep the same allocation to stocks.

That’s what’s genius about this framework: it not only explains why stocks go up over the long term, but it also links portfolio allocation decisions to stock market performance. In other words, if investors have temporarily overallocated to stocks and need to adjust lower, stock prices will go down.

This indicator can even explain things other valuation models can’t – like, say, the bull market of the 1980s. What happened back then was puzzling: prices skyrocketed in a period when interest rates were high and earnings contracted. Traditional models justified the rally by pointing to investors’ “irrational exuberance”, but the real reasons lay elsewhere.

First, prices had to rise to match the significant increase in the total value of liabilities during that period. Second, investors were massively underweight stocks at the time: numbers show their average stock allocation was only 20%. So when investors rebalanced their equity allocation to a more acceptable level, prices had to rise. And they did.

What does thecurrentforecast look like?

Investors' average stock allocation is currently 46%. That’s better than it was a year and a half ago (when it was 50% – the second highest reading history) but still above that dreaded 40% threshold. So unless investors permanently hold a higher allocation of stocks (which is possible, but unlikely), stock prices will decrease (although only slightly) over the coming decade, according to this indicator.

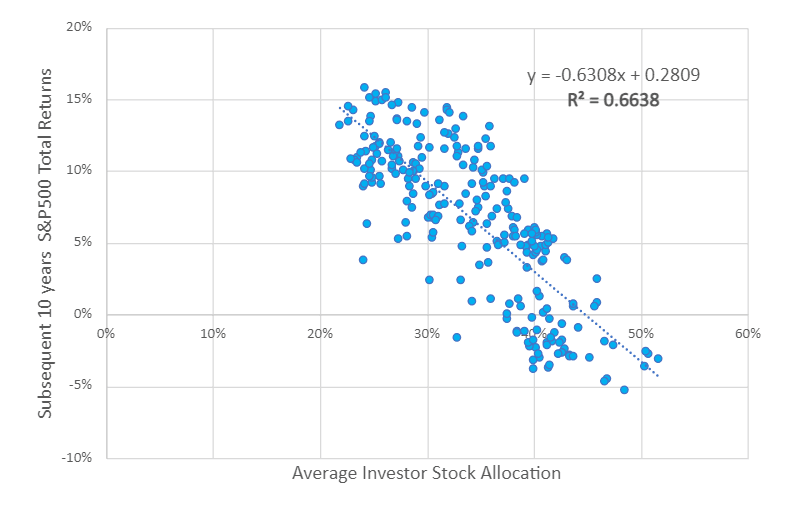

This chart shows the average investor stock allocation (horizontal axis) and the total returns for that investment over the following 10 years (vertical axis). Sources: Philosophical Economics blog, Federal Reserve Economic Data (FRED), Finimize. Past performance is not a guide to future performance.

As for whether that should worry you… well, yep: this indicator does indeed look like the best predictor of future stock returns. Historically, it’s predicted the S&P 500’s future 10-year returns better than any other, much more common valuation metrics – price-to-earnings (P/E) ratio, CAPE ratio, market cap to economic growth, or the Fed model, to name a few. And, sure, it may be different this time (you know, AI), but you should probably take its warning seriously. At the very least, add this “average stock allocation” number to your watchlist…

What’s the opportunity here?

You could use this as a contrarian timing indicator. If the average stock allocation is below 40%, you can breathe easy: it’s not too extreme and you’re better off buying and holding stocks. But if it’s above 40% – and remember, it’s at 46% right now – you could reduce your stock allocation, and keep it there until investors’ stock allocation falls back below the 40% mark. And remember, these indicators are like a slow cooker: they're best at predicting what will happen over the long term. So, don't give up and keep lifting the lid on that pot: they won’t tell you what will happen in 2024 or 2025.

Stéphane Renevier is a global markets analyst at finimize.

ii and finimize are both part of abrdn.

finimize is a newsletter, app and community providing investing insights for individual investors.

abrdn is a global investment company that helps customers plan, save and invest for their future.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.