Why Ashtead shares surged 180% since March to record high

Investors like Ashtead, even after a dive in fourth-quarter profit. Our head of markets explains why.

16th June 2020 10:01

by Richard Hunter from interactive investor

Investors like Ashtead, even after a dive in fourth-quarter profit. Our head of markets explains why.

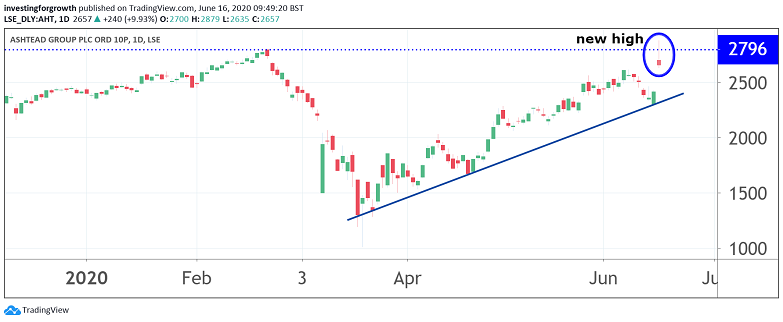

FTSE 100 equipment rental company Ashtead (LSE:AHT) has so far seen off most of the pandemic challenges with aplomb. And, in response to its latest update, the shares traded as high as 2,876p Tuesday. In March, they were worth little more than a tenner.

As expected, the fourth quarter performance teetered as the full force of the virus became apparent, with economies and markets reacting accordingly. Until that point, Ashtead had been progressing strongly, and revenues for its US Sunbelt business, which accounts for 86% of group revenues and 96% of profits, reflect the initial hit. Revenues had risen 3% year-on-year in March, which was followed by a 12% decline in April and 14% in May.

At the same time, Ashtead continued to pursue its policy of bolt-on acquisitions, especially in the US, resulting in an additional £453 million spend and contributing to a net debt figure which currently stands at £5.4 billion, an increase of 43% compared to the previous year.

Given the company’s exposure to the US in particular, the fragility of the construction market is of some concern not only in the present, but potentially further out as the speed and the breadth of easing restrictions come through at an uneven pace.

Source: TradingView. Past performance is not a guide to future performance.

Even so, there are two major strands which have lifted the spirits of investors following this announcement for the period ended 30 April 2020.

From a reporting perspective, the strength of momentum over the first three quarters of the year has largely enabled Ashtead to get over the line for the full year. Overall, revenues grew by 9%, the group consolidated its access to liquidity which now stands at some $4.6 billion, and the fact that Ashtead was designated as an essential business in its major markets cushioned some of the wider economic blow.

Meanwhile, the group maintained its high operating margins and, despite a decline of 15% in US rental revenue income in just five weeks – an indication of the speed and scale of the pandemic – has emerged in a strong financial position. The group has maintained its progressive dividend policy and, while the yield of 1.7% is not punchy, it nonetheless adds to over a decade of dividend growth.

This has been made possible by the second of Ashtead’s achievements, namely to have taken swift and decisive action at an early stage. In the first weeks of March, the company decided to slash capital expenditure, suspend the share buyback programme, pause any further Merger and Acquisition activity and bear down on operational costs.

Alongside the company’s cash generative ability, this has had the desired effect of largely stemming a flow which has had such a detrimental impact on other companies in the current environment. Indeed, the diversity of the sectors to which Ashtead is exposed has already provided some benefit as different parts of the economy have performed in differing ways.

- The fund I sold after a 22% rally

- ii view: Can BP dividend survive switch to greener world?

- Take control of your retirement planning with our award-winning, low-cost Self-Invested Personal Pension (SIPP)

The resilient showing from the business has been mirrored by a share price which has remained stable in the year to date, has risen 86% since the indiscriminate markdowns leading to the March lows, and is ahead by 24% over the last year, as compared to a decline of 17% for the wider FTSE 100 index.

The company appears to have taken the right decisions at the right times and is well-placed, despite the challenges which are yet to come as a result of the pandemic. Ashtead has been a market favourite for some time and the consensus of the shares as a ‘buy’ will almost certainly remain intact.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.