Multi Asset: what patterns of market returns can tell us

13th April 2023 10:07

by Max Macmillan from Aberdeen

What’s really happening in the global economy? Looking at the cross-asset pattern of returns may help us find out.

Interpreting what’s priced into markets is just as important as getting the outlook right. Only by correctly assessing what’s already discounted – or implied – can we judge how market expectations are likely to change, the returns that will ensue, and know how to position in funds.

But how can we know what markets believe about the future, and what is already in the price?

Pattern of returns

When we forecast market returns under different plausible scenarios, the correlation structure, or pattern of relative moves across asset classes, is determined by the nature of the macro shock.

A hawkish Federal Reserve (Fed) shock – a scenario in which monetary policy is tightened – will see a simultaneous selloff in government bonds and corporate risk (equities and debt), typically associated with dollar strength.

Conversely, in the case of a downside shock to prospective economic growth, the pattern is typically for bonds to perform even as corporate risk sells off, with weakness in commodities.

Understanding how the changing macro environment affects assets, through its impact on market expectations for growth, inflation, and the setting of monetary policy, can help investors know what asset allocation to deploy for different scenarios and phases in the economic cycle.

Hunt for mispricing

But this process can also be reversed – to extract from markets information on what they’re currently discounting. No investment is possible on an outlook alone. We must also be able to gauge what the starting point is.

In this sense, it’s mispricing in financial markets – the gap between what’s priced and what we expect to happen – that we position for, not simply for assets that we ‘like’.

Knowing whether an investment represents good value implies an evaluation of the price paid for it which, in financial markets, means an understanding of the outlook it is discounting.

Hot air balloon

Analysing the market’s pattern of returns is the best way to determine what macro environment is getting discounted. To this end, a hot air balloon is more useful to us than a microscope.

For while there can be a multitude of reasons why an asset, or asset class, is going up or down in price, there are only limited macro factors that can explain the overall pattern of relative moves markets experience at any point in time.

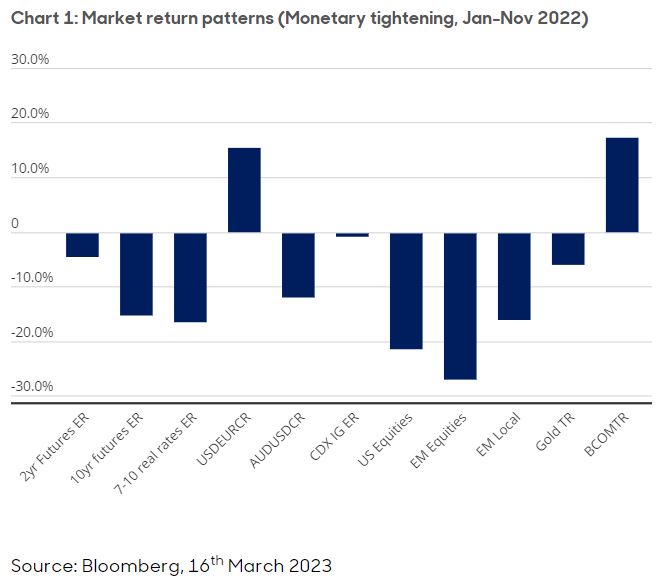

Case study: pattern of returns in 2022

In 2022, even as the Fed and other developed market central banks woke up to their policy mistake a year earlier – they’d wrongly considered nascent inflationary pressures to be transitionary – the pattern of returns was characteristic of a hawkish policy shock.

How it started…

Last year’s simultaneous selloff in bonds and equities, accompanied by dollar strength, was no anomaly. The speed of the interest-rate hiking cycle was certainly a shock to markets, but the market impact was, in fact, characteristic of this monetary-policy macro driver (See Chart 1).

Commodities were able to deliver positive performance during this period, partly due to the war in Ukraine and its supply-side effect, but also because they are not immediately sensitive to the rates-driven de-rating that other financial assets suffer. Instead, it’s typically only when underlying economic activity weakens that they fall in value.

This pattern of returns belied the once-prevalent narrative that recession fears were driving markets – something quite inconsistent with the fact that expected-earnings growth remained positive during this period – and the entire shock to US equities was driven by an interest-rate related fall in the valuation multiples.

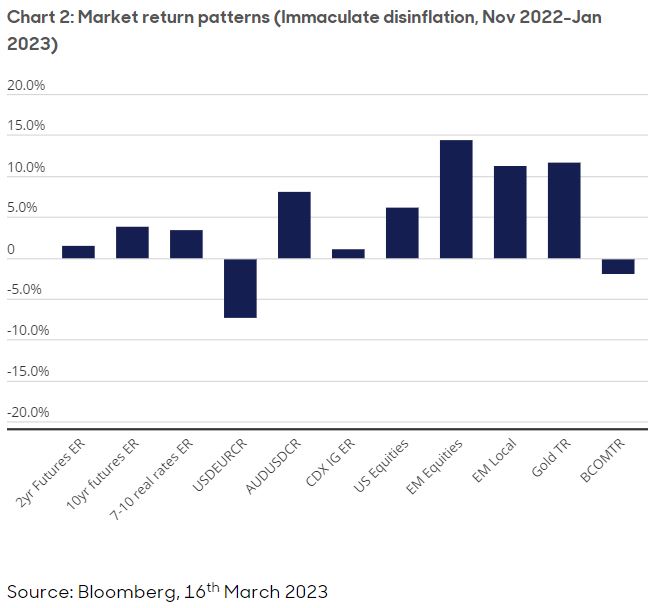

…turning point

Late last year, as inflation showed clearer signs of having peaked and the Fed softened its language to guide the market towards a slowdown in the pace of hikes, bond-market volatility retreated. The pattern of market moves then exhibited the opposite of the earlier policy-normalisation phase – bonds and equities rallied back. Amid dollar weakness, emerging market risk outperformed US risk (See Chart 2).

Again, an understanding of the macro drivers of this return pattern (notably a partial unwinding of the hawkish shock that predated it) helped belie the notion that it was a positive-growth shock (perhaps due to the China reopening) that was getting discounted. A positive-growth shock would have seen equities perform even as bonds sold off (which was not the case).

The entire year was thus driven by the market pricing of the magnitude of policy hawkishness, driving a ferocious de-rating in the first part of the year and an enthusiastic re-rating afterwards, all the while retaining the positive correlation between bonds and equities (when both asset classes move in tandem).

Looking ahead

From an optimistic starting point – with assets having re-rated and discounting something akin to a soft landing (or no landing) in 2023 – market pricing remains vulnerable to any cracks appearing in the economy as a consequence of last year’s aggressive policy normalisation.

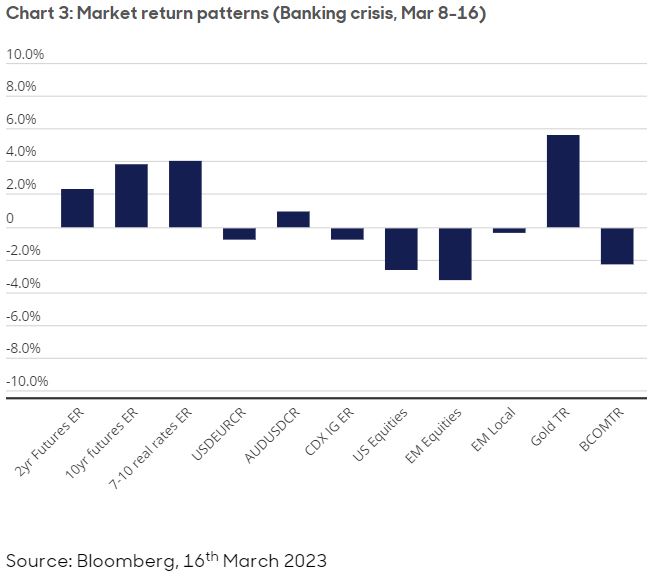

The most recent escalation of perceived risk surrounding US bank failures and the capitulation of a Swiss banking giant shocked markets into a more typical risk-off pattern of returns – one that implies a downward shock to growth, sees interest rates cut and corporate earnings fall.

From early March to the time of writing in mid-March, bonds rallied aggressively as equities and other corporate risk sold off, commodities fell, and the dollar rallied versus most currencies except the Japanese yen (see Chart 3).

At long last, bonds are providing an offset to equities. With demand fears taking over from monetary policy as the key market driver, the negative correlation between bonds and equities (when one goes up the other falls) is, at least temporarily, restored. We can see how the prospects of a recession are now creeping into the pattern of market returns.

These sort of changes to the correlation structure of markets do not determine the future, but they can be early indicators of a changing macro environment, and they tend to lead the publication of hard economic data.

Given our expectation that 2023 will see a recession in developed markets, we think this pattern correctly anticipates larger, but similar, moves occurring over the next 12 months.

Max Macmillan is Head of Strategic Asset Allocation Research at abrdn

ii is an abrdn business.

abrdn is a global investment company that helps customers plan, save and invest for their future.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.