Macro and markets: good news is bad news in US inflation fight

12th April 2023 10:06

by Abigail Watt from Aberdeen

Abigail Watt explains why we think US monetary policy will continue to target inflation in the coming months, leading to a US recession starting in the third quarter.

Improving economic data at the start of this year would normally be good news for financial markets, which have been plagued by recession fears in recent months.

But with few signs that the inflation backdrop is improving, strong growth risks fuelling the underlying imbalances that drive prices higher in the US economy.

This has created a dilemma for the Federal Reserve (Fed). Recent financial stability concerns following the failure of Silicon Valley Bank make it more difficult to raise interest rates further to fight inflation.

However, we expect the Fed may need to continue doing so and US monetary policy tightening is likely to drive the US economy into recession by the third quarter.

Expect a pivot to easier policy only when recession takes hold. This is to support the economy through the downturn. Our forecast is for US rates to eventually return to zero.

This is our base, or most likely, scenario. It’s important because US monetary policy and long-term economic health affects economies and financial markets elsewhere.

Multiple scenarios

To illustrate the key judgements behind our base case we can compare it with three alternative scenarios for the economy.

These scenarios can be thought of as logical outcomes linked to different answers to two questions about the economy: ‘is a recession necessary to quell inflation pressures?’; and ‘has the Fed’s policy tightening until now been sufficient to induce a recession?’.

Here are the alternative scenarios:

‘Fed has two bites of cherry’ describes a situation in which a recession is necessary, but monetary policy isn’t sufficiently tight to cause one. It would merely delay the pain of a recession.

That’s because underlying inflation pressures would remain unchecked, and the Fed would likely be forced to tighten further in a second attempt.

While this may lead to a relief rally in the near term, when markets reprice for the higher terminal rate given stubborn inflation pressures, both risk assets and fixed income would underperform.

A ‘Soft landing’ is possible but only when a recession isn’t necessary to bring inflation down. This allows the Fed to tighten policy just enough to return inflation to its 2%-target without causing a recession.

While not impossible, history tell us that this is unlikely. Supply-side factors, such as labour force participation, would have to improve significantly so that a large correction to employment and activity isn’t necessary.

This is clearly the best outcome for risk assets with inflation returning to target and growth stabilising.

‘Whoops!’ is the final scenario and the worst outcome for the Fed. Here the central bank tightens policy and pushes the economy into a recession, but inflation pressures were already on their way out.

This would be a clear policy mistake leading the Fed to fail in both of its mandates – as the economy slips below full employment and inflation undershoots 2%. This would lead to quicker loosening of policy.

Risk assets would likely underperform within the depths of recession, but the strong loosening in policy would ultimately lead to a recovery in markets given expectations of an economic rebound.

The path ahead

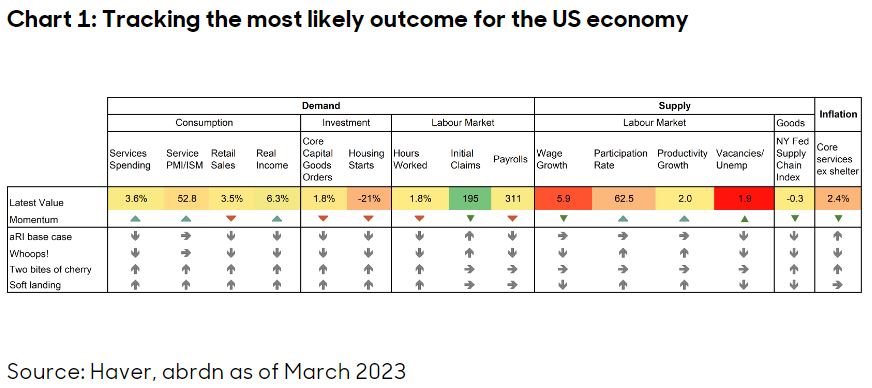

To help answer these two vital questions about the economy we can track the key moving parts in the US economy (see Chart 1).

Our analysis shows the momentum in each data series, and the direction in which the data need to move for each of the different scenarios to occur.

Considering some of the key indicators in turn:

- The strength of the consumer seems to be consistent with a ‘Two bites of the cherry’ or ‘Soft landing’ outcome for now. However, the effects of policy tightening on consumption can take time, so it’s hard to know how quickly this strength will fade.

- Investment spending, which is more interest-rate sensitive, has been weak and so it’s tracking in line with our recessionary base case.

- The recent softening in hours worked may signal some loosening in the labour market with employers reducing hours, instead of cutting back on workers.

- Wage growth is still too high to be consistent with the Fed’s inflation target and the participation rate is well below the pre-pandemic average.

- The number of vacancies per unemployed person, something that is closely watched by the Fed, is proving sticky at 1.9. This decreases the likelihood that declining vacancies can resolve labour-market imbalances without a rise in the unemployment rate.

- Progress continues to be made on goods inflation. The New York Federal Reserve’s supply chain index indicates further easing in earlier supply-chain bottleneck issues.

- Core services inflation (excluding rents) accelerated again in February and there are signs that, despite some loosening in the labour market, inflation pressures on the services side remain sticky.

With the data showing a mixed picture, monitoring how these progress in real time will be important to figure out whether our base case is being realised, or whether a different path for the US economy will become more likely.

Implications for investors

The only true positive outcome for markets is if a recession isn’t necessary and the Fed doesn’t inadvertently cause one. Only these outcomes are compatible with a soft landing – reflected in rapidly moderating inflation and solid economic activity.

The near-term data flow will therefore be critical for the monetary policy and financial market outlook. We think that stronger economic data will lead to a higher terminal rate.

This will be in spite of the recent turbulence in markets caused by investor concerns over bank stability, which has led to a risk-off environment.

The bottom line is this – the Fed still has more work to do to bring inflation back down to target and it musn’t be distracted from this goal.

Abigail Watt is a Quantitative Research Economist at abrdn

ii is an abrdn business.

abrdn is a global investment company that helps customers plan, save and invest for their future.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.