House view: investing in a shifting economic landscape

Four of abrdn’s most senior investors give their top ideas for the rest of 2024 and beyond, based on abrdn’s latest global outlook. Do you agree with their choices?

3rd July 2024 11:39

by Aberdeen Investments from Aberdeen

Investing in a shifting economic landscape is daunting. You’re being asked to make big decisions even as you struggle to make sense of new surroundings. Last week more than 145 abrdn clients from around the world gathered in a central London hotel to listen to what some of our most senior people had to say about this dilemma.

We didn’t offer a map to buried treasure, but what we did do was remind everyone that even as we’re grappling with uncertainty – Have we beaten inflation? Is China on the mend? Who will be running the US next year? – investors do have options.

Peter Branner, chief investment officer, led Russell Barlow, global head of multi asset and alternative solutions; Anne Breen, global head of real estate; Paul Diggle, chief economist; Devan Kaloo, global head of equities; and Craig MacDonald, global head of fixed income, in a discussion on what a shifting landscape means to each of them.

Most importantly, given our macro views on what could happen over the next 12 months, our panellists offered their top tips on the most attractive investment opportunities in their respective asset classes.

Here are the edited highlights of that discussion:

A shifting landscape

Inflation pressures re-emerged earlier this year in the US and elsewhere, but we expect them to moderate on a month-on-month and quarter-on-quarter basis. This will give central banks room to cut interest rates further, and we see a gradual easing of monetary policy around the world this year. That’s one reason why, at the highest level, the House View favours both fixed income and equities. But there are risks to this forecast on several fronts, including geopolitical uncertainty.

China faces significant challenges. The property sector remains troubled and consumer confidence is low. Its population is ageing, and another Trump presidency would further strain relations with the US. But talk of slipping into the ‘middle income trap’ ignores the speed of technological innovation occurring in China. Comparisons with Japan’s ‘lost decades’ of deflation are off target. There are also signs that government stimulus is working, putting the economy on a trajectory to meet this year’s ‘around 5%’ growth target.

A Biden-Trump rematch in the US election later this year promises very different outcomes. The incumbent, Joe Biden, must battle negative voter perceptions of US economic conditions. If he succeeds, we can expect broad policy continuity. His opponent, who is marginally ahead in the opinion polls, would create more uncertainty. Donald Trump’s stated tariff, fiscal, regulatory and immigration objectives, if pursued, risk driving inflation back up.

Looking further ahead, we need to reassess some long-held assumptions because of structural changes in the global economy. Expect to see higher inflation volatility due to supply shocks caused by geopolitics, climate change and even future pandemics; no return to negative interest rates; globalisation shifting towards industrial policy and supply-chain security; and transformative change from artificial intelligence.

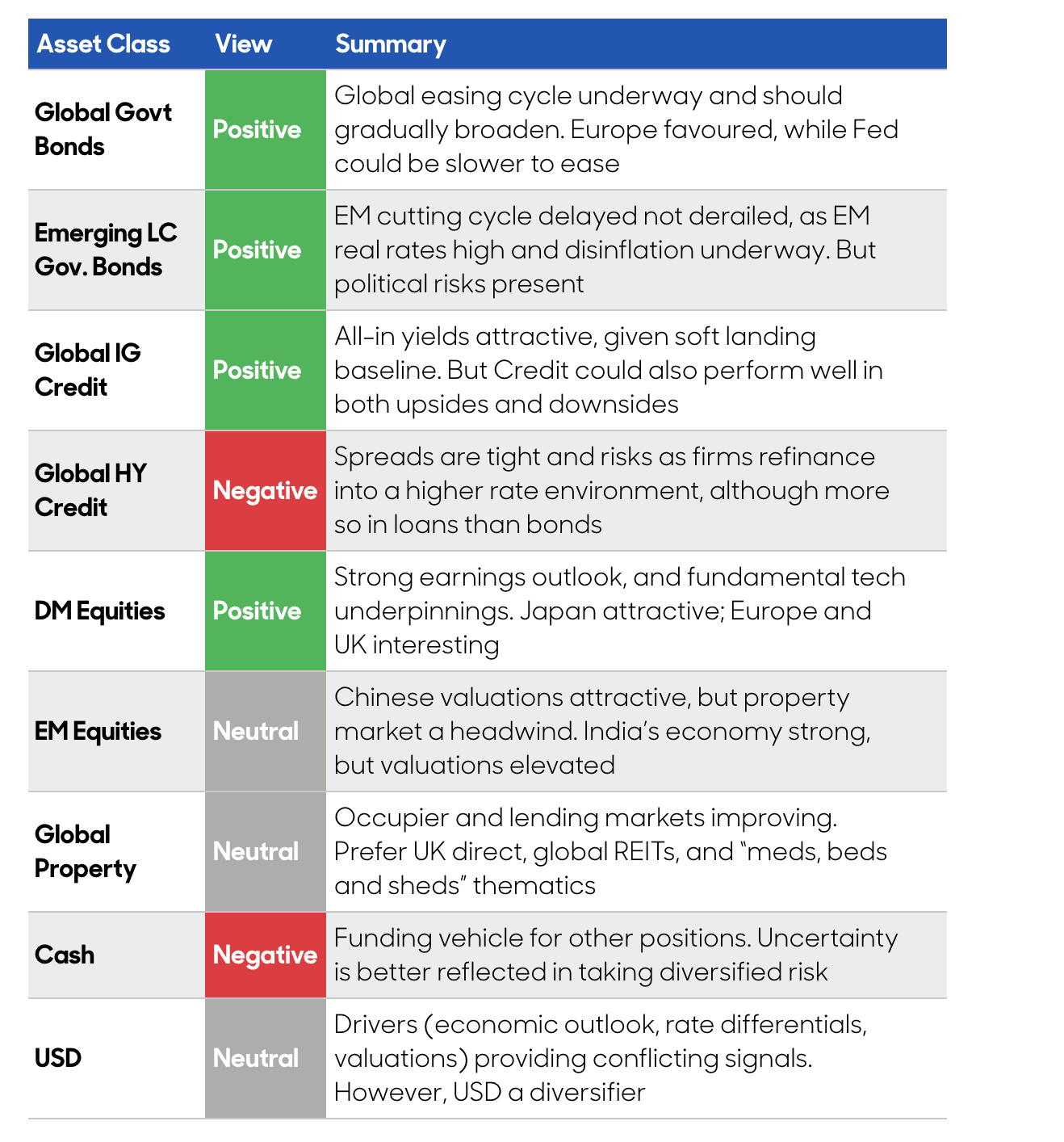

abrdn House View

Source: abrdn, June 2024. The views expressed should not be construed as advice or an investment recommendation on how to construct a portfolio or whether to buy, retain or sell a particular portfolio investment.

What’s the investment opportunity?

Peter challenged the global heads of asset classes to distil their views into a handful of ‘high conviction’ investment ideas. Here’s what they came up with:

Fixed Income

- Emerging markets will do well if our base case scenario – inflation and interest rates come down, the global economy normalises – plays out. Duration makes sense.

- But if you’re worried about Trump, if you’re worried about sticky inflation – short-duration credit makes sense because corporate balance sheets are good and bond yields are high.

- You can have variations between the two views depending on your risk appetite. But do expect volatility over the next 12 months.

Equities

- Thematically, we like the intersection between technology and climate change. There are interesting things going on in electrification. Similarly, around AI, and the rise of artificial intelligence.

- Geographically, we like Europe (including the UK). Interest rates will come down and these markets should recover. Most importantly, there’s a shareholder-return story happening at the company level in both markets.

Multi Asset & Alternatives

- Downside protection on risk assets looks attractive right now. Put options on the S&P 500 are one expression of this observation. Equity volatility is at historical lows. When coupled with high interest rates, this means the pricing of so-called 'out of the money' options is very attractive.

- There's a lot of support for the view that the US economy will achieve a soft landing. But if you’re worried about the geopolitics or feel the soft-landing narrative is fully reflected in market prices, buying protection via derivatives would be a cost-effective way to hedge those risks. The cost of protection on individual stocks remains high but given the stock concentration within the S&P 500, it's a very efficient way to hedge the risks posed by the biggest US technology companies.

- Gaining passive exposure to hedge funds gives you a more economical way to access the industry return and to express top-down strategy and sub-strategy views. We see equity-related strategies and some of the asset-backed strategies, within the fixed income space, looking attractive.

Real Estate

- Global REITs, at this recovery stage in the cycle, are very attractive. Real estate investment trusts have the potential to perform even better than many stock markets over the short term.

- Investing in buildings to meet demand for ‘living’ space is attractive over the medium term because there isn’t enough good-quality accommodation for people in most cities around the world.

- Real estate infrastructure – energy ecosystems in buildings, connectivity, the generation and storage of power – will drive future performance.

ii is an abrdn business.

abrdn is a global investment company that helps customers plan, save and invest for their future.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.