Global dividend investing – growth with resilience

2nd August 2023 13:56

by Josh Duitz from Aberdeen

Josh Duitz, abrdn's Head of Global Equities, explains why he thinks global dividend investing is well suited to current economic conditions.

Dividend investing strategies have a reputation for providing attractive long-term returns, and in particular, attractive long-term risk-adjusted returns. This is due to their defensive advantages, including less downside volatility in weaker market conditions on average. However, the specific conditions of any given economic cycle also matter greatly, as does the type of dividend strategy being pursued.

In this article, we make the case that a dividend investing strategy that focuses on companies that consistently grow their dividends works well in the context of global equities. We also make the case for why such a dividend strategy can offer a powerful combination of growth with resilience, which may be particularly well suited to the prevailing global economic environment of slowing growth, elevated inflation and higher interest rates.

Superior long-term returns

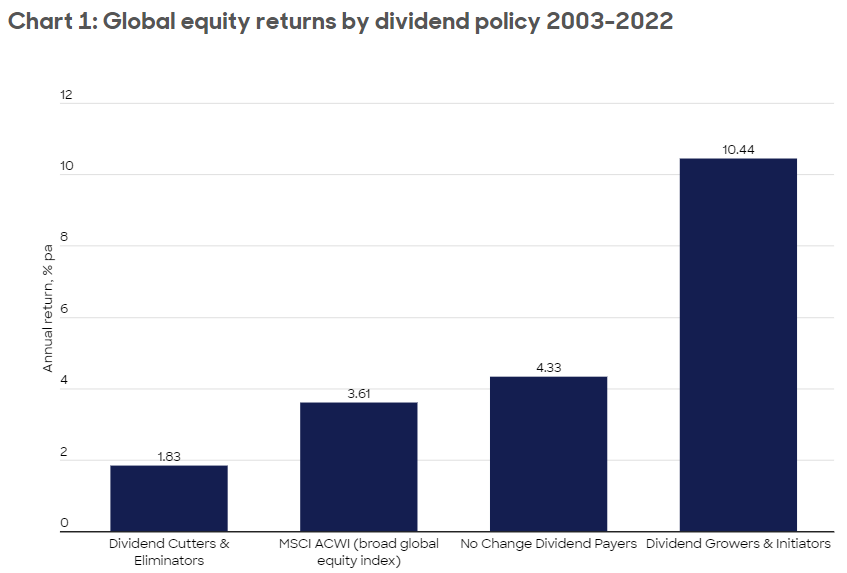

There is substantial evidence from across different equity markets showing that dividend-orientated investing strategies outperform the broader market over the long run. Chart 1 below shows that over the last 20 years, no-change dividend-paying global companies (i.e. those that have just maintained their dividends without either raising or cutting them) have comfortably outperformed broader global companies, as represented by MSCI ACWI index.

However, the stand-out performance has come from companies that have initiated or consistently grown their dividend payments. Indeed, this segment’s annual return over the last 20 years is nearly triple that of the broad global equity index return.

Source: abrdn, Factset. Data from 31/12/2002 to 31/12/2022. Historical compounded returns (%) of dividend categories and standard deviation (%) since 1993. The investment universe is the MSCI All Country World Index, using annual income class returns.. Dividend policy constituents are calculated on a rolling 12-month basis and are rebalanced annually. Category returns are calculated on a monthly basis. Shown for illustrative purposes only. Index returns do not reflect any management fees, transaction costs or expenses. Indices are unmanaged and cannot be invested in directly. For illustrative purposes only. Past performance is not indicative of future returns.

Dividend policy categorisation explanation: The ‘Income Growers & Initiators’ category represents performance for companies which either increased or initiated dividend distributions. The ‘No Change Dividend Payers’ category represents performance for companies which pay a dividend but have neither increased nor decreased their dividend distribution. The ‘Dividend Cutters & Eliminators’ category represents performance for companies which have either cut or eliminated their dividend distribution.

Further indicating the importance of dividend directionality, Chart 1 above shows a marked underperformance in the returns of companies that have cut or eliminated their dividend payments.

Lower volatility

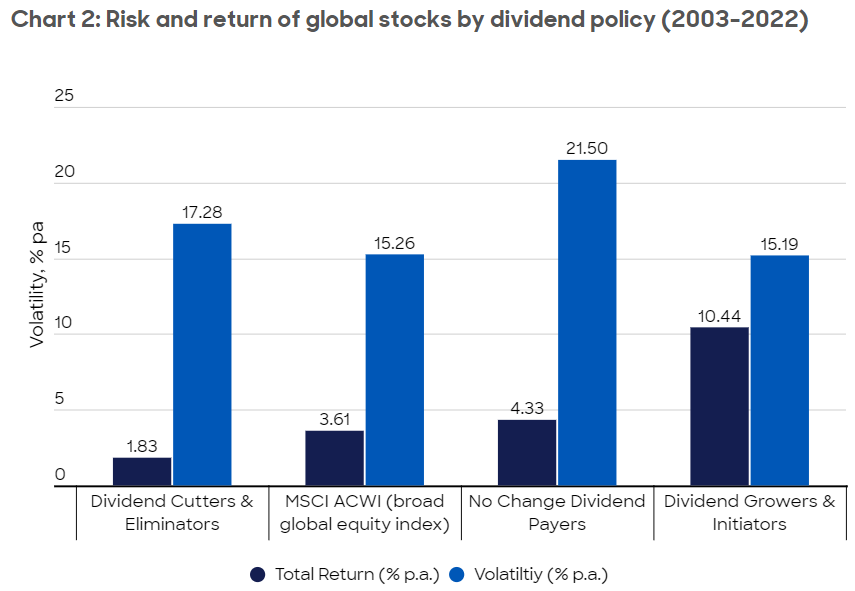

The other main attraction of dividend investing comes from the risk perspective – namely lower volatility, which has contributed to historically attractive risk-adjusted returns over the long run.

Chart 2 below shows that within global equities, the annual return volatility (lighter blue bars) of ‘dividend-growers and initiators’ is lower than ‘dividend-cutters and eliminators’, and considerably lower than ‘no-change dividend-paying’ companies. Relative to broader global equities too (i.e. the MSCI ACWI index), over the last 20 years, the return volatility of dividend-growers and initiators has also been slightly lower, contributing to better risk-adjusted returns.

Source: abrdn, Factset. Data from 31/12/2002 to 31/12/2022. Historical compounded returns (%) of dividend categories and standard deviation (%) since 1993. The investment universe is the MSCI All Country World Index, using annual income class returns. Dividend policy constituents are calculated on a rolling 12-month basis and are rebalanced annually. Category returns are calculated on a monthly basis. Shown for illustrative purposes only. Index returns do not reflect any management fees, transaction costs or expenses. Indices are unmanaged and cannot be invested in directly. For illustrative purposes only. Past performance is not indicative of future returns. For dividend policy categorisation explanation please see source wording under Chart 1.

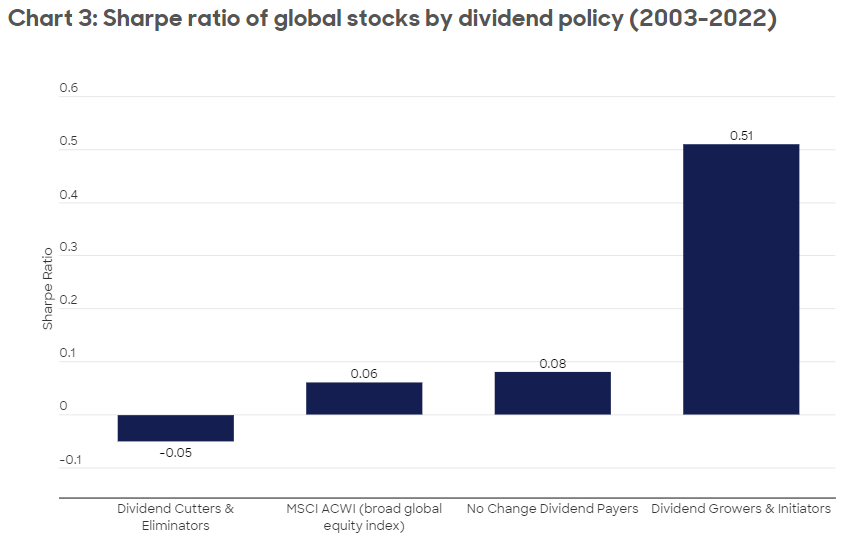

While the side-by-side depiction of annual returns versus annual volatility as shown in Chart 2 above is useful, a more precise and comparative measure of returns versus risk is available from a Sharpe Ratio perspective. As shown below in Chart 3, on this measure, the superior risk-adjusted returns of the dividend-growers and initiators segment is striking.

Source: abrdn, Factset. Data from 31/12/2002 to 31/12/2022. The Sharpe Ratio measures risk-adjusted return by dividing the excess return above the risk-free rate by the standard deviation of the portfolio return. Risk Free Rate - from 01/01/22 SOFR, prior to this, 3-month USD LIBOR. Historical compounded returns (%) of dividend categories and standard deviation (%) since 1993. The investment universe is the MSCI All Country World Index, using annual income class returns.. Dividend policy constituents are calculated on a rolling 12-month basis and are rebalanced annually. Category returns are calculated on a monthly basis. Shown for illustrative purposes only. Index returns do not reflect any management fees, transaction costs or expenses. Indices are unmanaged and cannot be invested in directly. For illustrative purposes only. Past performance is not indicative of future returns. For dividend policy categorisation explanation please see source wording under Chart 1.

Sources of risk advantage

The lower volatility of dividend strategies, which has given them a defensive reputation, can be linked to certain qualities that are often found to be prevalent in the typical profiles of companies that pay dividends and grow dividends. Indeed, the ability to pay dividends regularly, and the ability to grow dividends, is in itself widely seen as an indicator of reliable earnings quality and growth.

The risk advantage of dividend strategies can also be linked to behavioral investing. In particular, in more challenging economic and market conditions, equity investors tend to prefer the increased certainty of dividend payments (which are inherently less risky and volatile than capital gains) and dividend cashflows which can provide a valuable cushion against potential capital weakness.

Behaviorally, on the companies’ side too, there is usually strong aversion to cutting dividends because of the potential negative signaling effects of doing so. This is something that also helps to explain the considerably lower year-to-year volatility in dividends payments compared to corporate profits.

Lower drawdowns in down markets

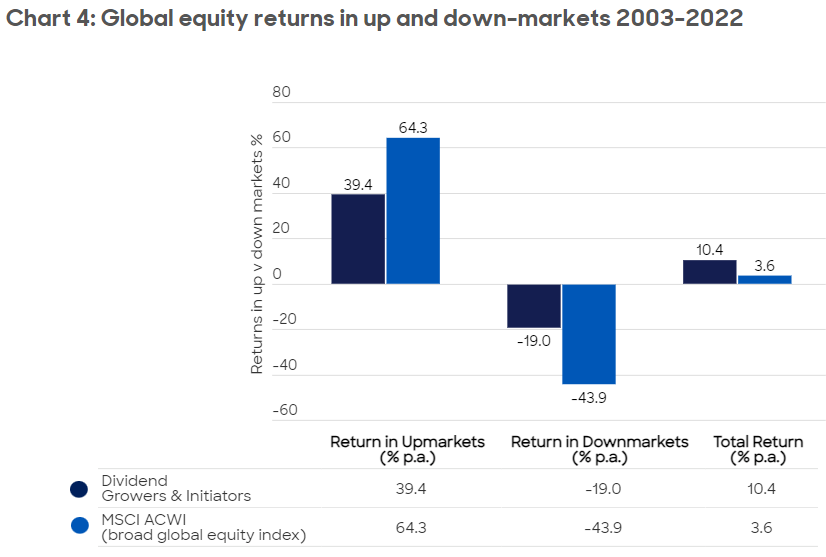

The above mix of behavioral factors is helpful for explaining the frequently observed pattern of outperformance of dividend strategies in down-markets.

Indeed, in the case of global equities, as shown in Chart 4 below, the drawdown in down-markets of the dividend-initiators and growers segment was less than half on average, compared to broader global equities over the last 20 years. Chart 4 does also show that dividend-growers capture relatively less of the upside compared to broader global equities during up-markets. However, the lower drawdowns of this segment trump the lower upside capture, resulting in substantial outperformance over the long run.

Source: abrdn, Factset. Data from 31/12/2002 to 31/12/2022. Historical compounded returns (%) of dividend categories and standard deviation (%) since 1993. The investment universe is the MSCI All Country World Index, using annual income class returns. The ‘Income Growers & Initiators’ category represents performance for companies which either increased or initiated dividend distributions. Dividend policy constituents are calculated on a rolling 12-month basis and are rebalanced annually. Category returns are calculated on a monthly basis. Shown for illustrative purposes only. Index returns do not reflect any management fees, transaction costs or expenses. Indices are unmanaged and cannot be invested in directly. For illustrative purposes only. Past performance is not indicative of future returns.

Inflation-protected income

Income from equity dividends has some specific well-known advantages compared to income from bonds. Firstly, albeit with more risk, equities typically offer greater upside potential from price appreciation. Secondly, unlike most bonds and other investments that pay set interest rates, companies have the ability to increase their dividend payments over time. As such, companies that increase dividends in inflationary environments can potentially provide inflation-hedged income opportunities.

The benefits of a global approach

Although dividend strategies have an understandable defensive reputation, the abundance of dividends across key sectors means there is also ample scope for diversification. As shown below in Chart 5, the global equities market (as represented by the MSCI ACWI Index) is especially well diversified across sectors and more so than some regional markets, which we think supports the case for a global approach to dividend investing.

Dividend investing today

Today’s global economic environment is for the most part characterised by high inflation and an unprecedented pace of interest rate rises aimed at addressing this. In turn, this is leading to markedly slower economic growth and an elevated risk of recession in many countries.

In this context, the surge in the ‘risk-free interest rate’ implies reduced investor preference for companies offering uncertain future growth, and an increased preference for solid earners, high dividend-payers and dividend-growers.

In the current environment of significantly higher interest rates and increased credit risk, balance sheet strength – another of the typical features of many dividend-paying and dividend-growing companies – gains added importance. Following on from this, it is our view that when it comes to executing a dividend-focused investment strategy, an active rather than a passive approach is better suited to identifying the totality of specific risks and opportunities.

Putting everything together

Global companies that grow their dividends tend to be well-established, high-quality companies with solid balance sheets, that also benefit from proven earnings and cash-flow resilience. Historically, over long periods, these types of companies have delivered good returns combined with lower volatility, resulting in strong risk-adjusted returns well in excess of broader global equities.

From a risk perspective, the defensive reputation of dividend strategies appears linked to increased investor preference for the typical profile of dividend-paying and dividend-growing companies in more challenging economic periods. In addition, dividend payments tend to be inherently more stable and certain, providing valuable downside protection that is also reflected in significantly lower drawdowns in down-market periods.

In summary, we believe the long-term case for dividend growth-focused investing in global equities is empirically well grounded. Furthermore, such an approach may appeal especially to investors looking for global equity market exposure, but with a greater degree of built-in resilience. However, from a more tactical perspective too, we believe that today’s economic backdrop (of high inflation, rising interest rates and weaker growth) appears well suited to a dividend growth-focused strategy in global equities.

Josh Duitz is Head of Global Equities at abrdn

ii is an abrdn business.

abrdn is a global investment company that helps customers plan, save and invest for their future.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.