Two stocks for traders seeking capital gains

After previously making good calls on this sector, analyst Rodney Hobson updates his view on these stocks which he had correctly predicted would fall. He thinks the next move is likely upwards.

19th March 2025 08:38

by Rodney Hobson from interactive investor

American housing stocks have suffered amid the political uncertainty that followed President Donald Trump’s inauguration. They look to have fallen far enough and could be due for a rebound, especially if this week’s better news on inflation is followed by another cut in US interest rates.

Let us be realistic. There are always uncertainties – investing would not provide opportunities if we all knew what was coming tomorrow – and there are more challenges than usual at the moment.

- Invest with ii: Buy US Stocks from UK | Most-traded US Stocks | Cashback Offers

A tariff war will almost certainly hurt rather than help American would-be homeownersand could well spark inflation that would delay or even reverse the downward trend in interest rates for new mortgages, despite Trump’s pressure on the rate-setting Federal Reserve Bank. Nor will wide-ranging sackings of federal employees do any favours for the US jobs market.

However, the American economy has held up pretty well since the pandemic and continues to perform better than other major economies, including China which is now resorting to the sort of stimulus measures that are not needed in Washington.

That should be of considerable comfort to shareholders in US housebuilders, despite a tailing off of house sales over the past few months, but an additional complication for investors is that, in such a large country, even the biggest operators work on a regional rather than a national basis and can be affected by regional as opposed to national factors.

D.R. Horton Inc (NYSE:DHI) is the largest housebuilder in the United States with markets across 36 states, so it is reasonably protected against a downturn in just one part of the US. Its shares hit $197 last September but are now down to $128, where the price/earnings (PE) ratio is derisory at only 9. Unfortunately for income seekers, the yield is still only 1.1%.

Source: interactive investor. Past performance is not a guide to future performance.

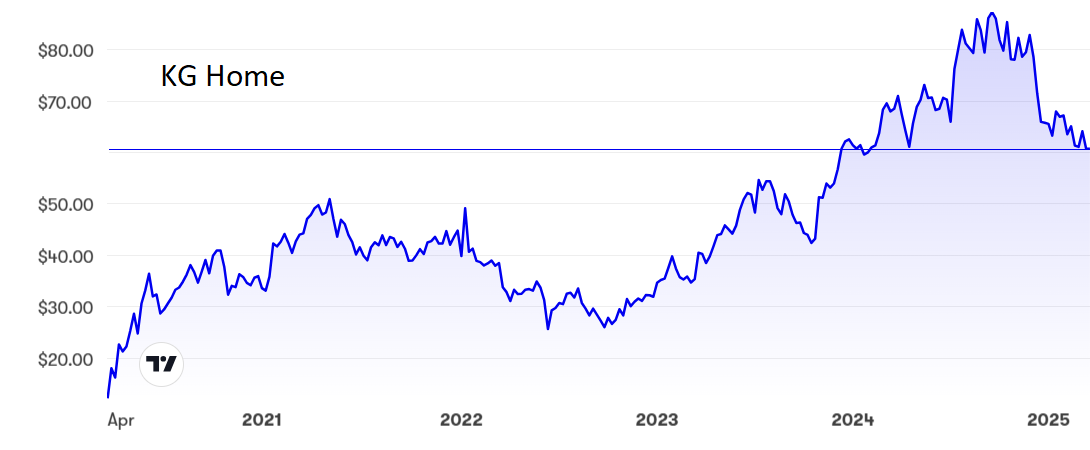

KB Home (NYSE:KBH), which operates on the West Coast and through southern states, is probably quite insulated from possible downturns in the manufacturing belt. Its shares have followed a similar trajectory to Horton’s, peaking at $90 but now down to $60. The PE is even lower than Horton’s at 7.2 but the yield is somewhat better at 1.6%.

Source: interactive investor. Past performance is not a guide to future performance.

Hobson’s choice: Anyone who bought DR Horton on my original tip at $71.50 three years ago has been consistently ahead, and my suggestion to take profits above $160 two years later is also looking good. My last comment in December at $167 was to hold off buying. This is still not a share for income seekers but traders looking for capital gains could certainly consider buying at the current price. The next move is likely to be upwards.

I have been less keen on KB in the past, but it too seems to be bottoming out so now merits a buy rating.

- Trump dump: biggest rotation out of US stocks ever

- How to invest like the best: Warren Buffett

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

Update: The metaphorical ink had scarcely dried on last week’s column when German sportswear group Puma SE (XETRA:PUM) revealed weaker sales than expected so far this year, blaming a “soft performance” in the US and China. Given that those two countries are the biggest economies in the world, that is particularly bad news.

Puma blames geopolitical tensions and trade disputes, two factors that may well get worse rather than better. So sales growth this year will be in single digits, and low to middle percent at that. Profits will be below €600 million (£504 million) compared with €622 million last year and a good €100 million less than analysts had hoped.

Of equal concern is Puma’s own failure to capitalize on the craze for retro trainers that has boosted rival adidas AG (XETRA:ADS). It has belated high hopes for its Speedcat range this summer but is playing catch-up rather than setting the pace. Such is the world of fashion, the new line may well arrive just in time to see tastes move on to some other must-have fad.

The warning prompted an initial 23% fall in the share price. Mercifully, I said last week that the shares were no more than a hold. It is a bit too late to advise shareholders to get out, but other investors should stay well clear.

Rodney Hobson is a freelance contributor and not a direct employee of interactive investor.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.