Stockwatch: four defensive shares to consider amid market wreckage

Global stock markets have been hammered in recent days, but some shares have become very popular. Analyst Edmond Jackson looks at some possible safe-haven UK stocks.

4th April 2025 11:40

by Edmond Jackson from interactive investor

When the market is having a serious fall over some macro issue, it is always interesting to see which shares hold up or even rally.

- Invest with ii: Open a Stocks & Shares ISA | ISA Investment Ideas | Transfer a Stocks & Shares ISA

Ominously, therefore, utilities had their best day in as long as I can remember – going back to the 2008 crisis possibly. It takes more than a sudden shock event – 11 September 2001, for example – to see the likes of National Grid (LSE:NG.), Severn Trent (LSE:SVT), SSE (LSE:SSE) and United Utilities Group Class A (LSE:UU.) rise in unison, but yesterday they all jumped around 5% amid savage falls generally.

Irony is how a utilities rally fills me with dread

I recall National Grid being a reliable “defensive” share during the early 1990s recession when 1980s’ excesses of corporate debt, overstretch and aggressive accounting saw many “growth” shares slaughtered. Otherwise, and taking the past five years as an example, it is a proxy for the volatile-sideways trend in most utilities:

Source: TradingView. Past performance is not a guide to future performance.

Generally, as investors, we have to hope yesterday’s surge proves no different from others on this chart, whereas a breakout to the upside would affirm a shift to bear market sentiment. So far today, however, National Grid has added another 1% to 1,065p.

Already, if utilities had just stayed firm or edged up a per cent or two yesterday, maybe fine, as if the market sensed Trump will walk back from the crazy destruction he’s unleashed. But concerted rallies of 5%-plus are as if a visceral fear has opened, amid uncertainty about where the chaos may lead economically in the medium term. It’s understandable given Trump’s tariffs exceed those introduced by the 1930 Smoot-Hawley Act, which played a part in the Great Depression. Today, nations are much more interlocked on trade than nearly a century ago.

- When markets fall, here’s what to avoid doing

- Last-minute ISA ideas for investors looking to ‘buy low’

But let us not lose sight of the essential matter: how market downturns are friendly to long-term investors, so long as your timing is reasonably right.

In my bones, and noting this utilities rally, I would be wary of cyclicals and indeed growth shares – unless their fundamentals truly appeal – until we see whether global recession can be averted. One forecast that I have seen is for the US to enter recession within 90 days as a consequence of effectively the biggest tax rise in US history. But let us see what actually unfolds.

‘Near-essential retail’ may offer more intrigue than utilities

A dilemma now with buying utilities – especially switching into the sector – is the potential for declines in common with zigzag charts, the moment sentiment shifts back to “risk on”. That is going to happen variously even through a bear market, hence you need to be an affirmed pessimist on the economy to raise utilities’ exposure to a meaningful 10% or more of an equities portfolio. There is a scenario where that works and, indeed, utility yields are meaningfully above 4% (albeit near fully paying out earnings which could change with tougher regulation).

As a first priority for defensive shares, I am more inclined towards the likes of FTSE 100 grocer Sainsbury (J) (LSE:SBRY), which at 242p (up 3% yesterday and a further 1% this morning) yields 6% with around 1.7x earnings cover according to forecasts. A forward price/earnings (PE) ratio of around 10x may be a slight premium to the underlying earnings trajectory and, of course, higher employment costs are manifesting. Yet the shares also currently trade around tangible net asset value, which should limit downside.

Setting aside the Covid roller coaster, the chart is at the low end of the past two years’ volatility:

Source: TradingView. Past performance is not a guide to future performance.

The obvious challenge is the continued expansion by Aldi and Lidl, compromising margin as the likes of Sainsbury’s get forced into price-matching. Lidl is also poised with another round of “veg for 15p” like last Easter to attract people for their big shop. Yet these German retailers have a limited produce range that the likes of Sainsbury’s exceeds at bigger stores.

- UK’s best supermarket stock named as price war looms

- A decade of pension freedoms: what you’ve done with your money

Coincidental with some flight to “near-essential retail” shares yesterday, mid-cap Currys (LSE:CURY) was able to release a “profits expected to be above previous guidance” update with five weeks of the financial year left. It was hardly a major upgrade, it being the median point of a profit range, implying near 7% and with the company’s broker raising the earnings per share target by 5% to 10.6p.

Yet the shares rose progressively throughout the day to close up 15% at 103p – on a 2.2% yield and circa 10x PE. In fairness, operating margins are only very slightly shy of Sainsbury’s, although electrical items have a somewhat more “discretionary” aspect of spending than groceries. There is a near-essential aspect to Currys’ sales range, although it’s in a highly competitive market.

The share’s re-rating is significantly explained by a turnaround in Currys’ Nordic region, although investors also possibly warmed to this being a second upgrade in 2025.

I rated Currys a “buy” at 57p in May 2023, similarly due to a positive update that implied its roller-coaster chart had fallen too far. The PE looked below 7x and yield over 5%. A private equity approach in February 2024 saw the shares finally start to rerate after a boom/bust pattern during Covid:

Source: TradingView. Past performance is not a guide to future performance.

My concern is how resilient Currys proves to be should US tariffs conflate with higher UK employment costs – and probably taxes later this year – for a recession. Grocery shares would then be more genuinely defensive.

So, Currys is a tricky call on this rally. News flow and the chart imply a momentum share, but the macro context can easily compromise that. Someone looking to nail a capital gain by 5 April might be justified with “sell”, but that looks harsh. I therefore compromise with “hold” while noting a variety of outcomes.

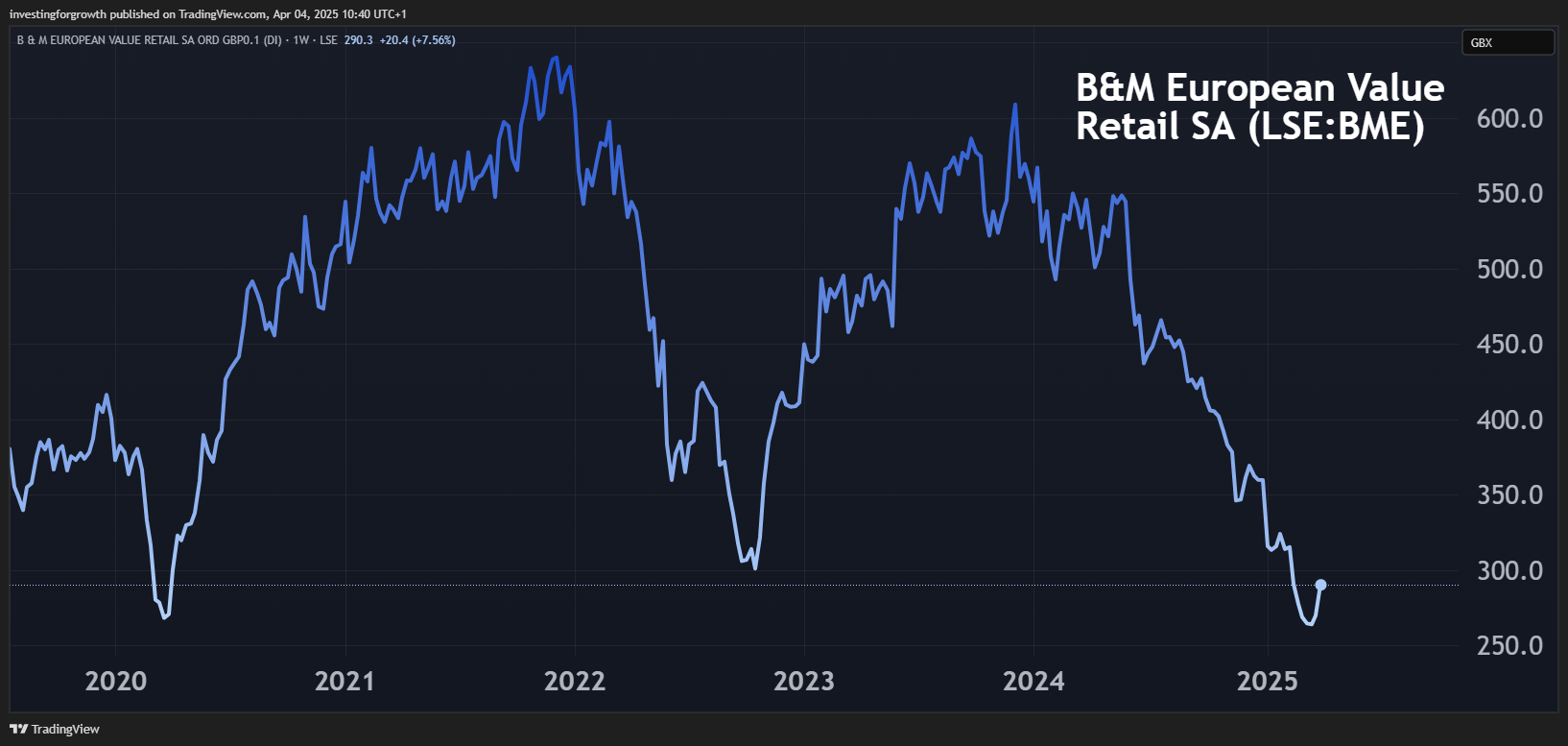

Mid-cap B&M European Value Retail SA (LSE:BME) is intriguing after a long fall from around 600p in late 2023 to 260p this March, then a rise of 9% to 283p in the first three days of April. There being no fresh news, the turnaround looks a blend of attempted bottom-fishing with a sense of how, in the current climate, “value” retail of grocery and mostly essential items should be defensive.

Source: TradingView. Past performance is not a guide to future performance.

I am also alert, however, despite its debts, that B&M is potentially a target for private equity ownership given a strongly cash-generative model. This was significantly why I drew attention to the shares at 279p last February, albeit concluding “hold” rather than “buy” given that the CEO had resigned and a newcomer might reset the business – possibly cutting dividends, where there has been a history of special payouts – to reduce debt. The September 2024 balance sheet also had negative net tangible assets.

- Stockwatch: is another retailer in takeover territory?

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

Its culture of recent updates is quite opposite to Currys, however, serially guiding profits down although by less than last February. Ostensibly, the yield is over 7% and PE around 8x, although this flags questions about whether B&M’s aggressive expansion in the UK and France can continue. Its chair did buy £201,000 worth of shares at 287p last February though.

The shares are thus in a “greed/fear conundrum” - they appear cheap but risks need clarifying. An update in respect of the year to 29 March is due on 15 April.

It is tempting to pull the trigger for “buy” here, given a risk that the shares continue to edge up, especially if a respected new CEO is confirmed and the update ceases to involve negatives.

In early dealings today, the shares added 1% to 286.5p versus the FTSE 250 index 0.5% easier - tacit evidence that B&M is with those defensive shares attracting buyers overall in this downturn. An averaging-in stance could work well, although strictly I should await more evidence on fundamentals, so therefore rate the shares a “hold”. You decide your risk appetite.

Edmond Jackson is a freelance contributor and not a direct employee of interactive investor.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.