Stocks are expensive: that doesn’t mean you should stay away

Stock prices are high right now, but that doesn’t necessarily mean you shouldn't buy them. To decide if they're good value for your portfolio, you just need to ask yourself a few simple questions. Let’s take a look.

12th January 2024 13:02

by Paul Allison from Finimize

At a 20x price-to-earnings ratio, the S&P 500 is well above its long-term average. That’s by no means a cheap valuation. But whether it’s a good or bad value for you depends on your view of the next few years.

So this is a good time to quiz yourself on the market’s five big yes-or-no questions. This speedy little test may just hold your answer to whether stocks are currently overpriced.

We’ll throw in a tiny markets history lesson too. Tech shares have done well lately, but their valuations are nowhere near where they were during the dot-com bubble in 1999.

It seems like everyone’s talking about how high stock prices are right now. And, let’s be real, they are. But that doesn’t necessarily mean you should stay away. Expensive stocks might still be a good value for your portfolio. To decide whether they are, you just need to ask yourself a few simple questions. Let’s take a look…

First things first: the basics and those questions.

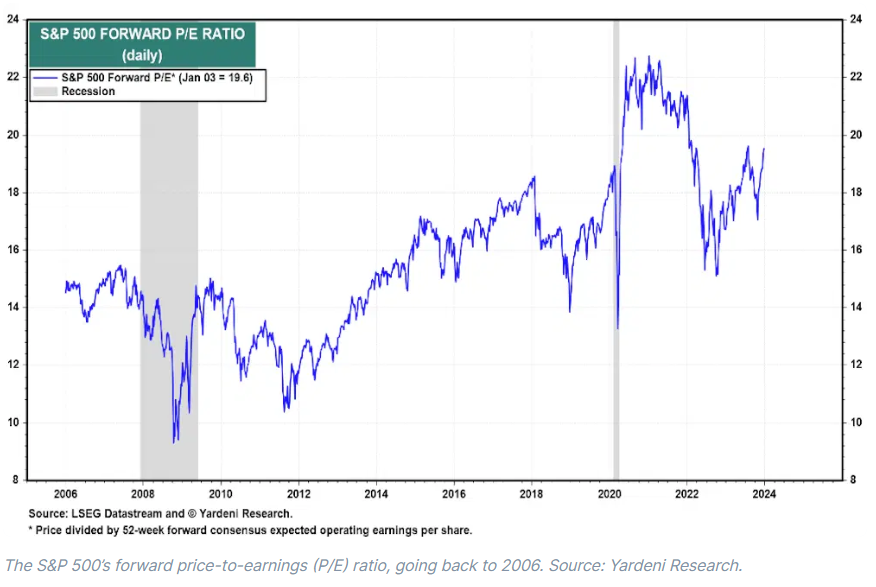

Okay, so the price-to-earnings (P/E) ratio is the most commonly used valuation measure out there. It divides the price of the stock by the earnings that analysts expect over the next 12 months. And, relative to its own history, this ratio is definitely in the nosebleeds – at least where the S&P 500 is concerned.

With a rip-roaring end to last year, the index’s price is up near 20 times analysts’ profit growth forecasts – and comfortably above its long-term average of around 17 times. So it’s no wonder some people are dissing US stocks as being too expensive. The thing is, it’s not as simple as that. The next 20 years will look different from the last, one way or another. So, when you’re investing, you have to take a longer-term view on what the future looks like.

Now, I’m not about to go deep here in explaining my expectations for the next two decades. Instead, I’ve come up with five questions that I think cover the “future” (or at least the next few years) pretty well. And, look, you don’t need to get overly scientific in your answers, just weigh these up using your own common sense and decide what’s most likely: yes or no.

Question 1: Do you think inflation will slowly creep lower from here?

Question 2: Do you think economies will avoid a recession, even if there’s an extended period of lower-than-normal growth?

Question 3: Do you think AI will accelerate company cost-cutting and boost economic productivity in the years to come?

Question 4: Do you think economies can cope with higher interest rates, and, do you think that maybe, in fact, higher rates might actually be a good thing?

Question 5: Do you think US companies will see profit growth over the next few years at least in line with their long-term average of 7%?

So, are you a bull?

If you answered yes to three or more of the five questions, you can conclude that valuation shouldn’t stand in the way of further US stock market gains. In fact, if you wanted to, you could even take this positive narrative a step further – throwing in the fact that US company profits have proved to be extraordinarily resilient and that perhaps valuations should be even higher than they are. After all, if Wall Street analyst forecasts are anything to go by, aggregate profit for the S&P 500 is set to grow at 12% this year, quite a bit beyond that long-term average.

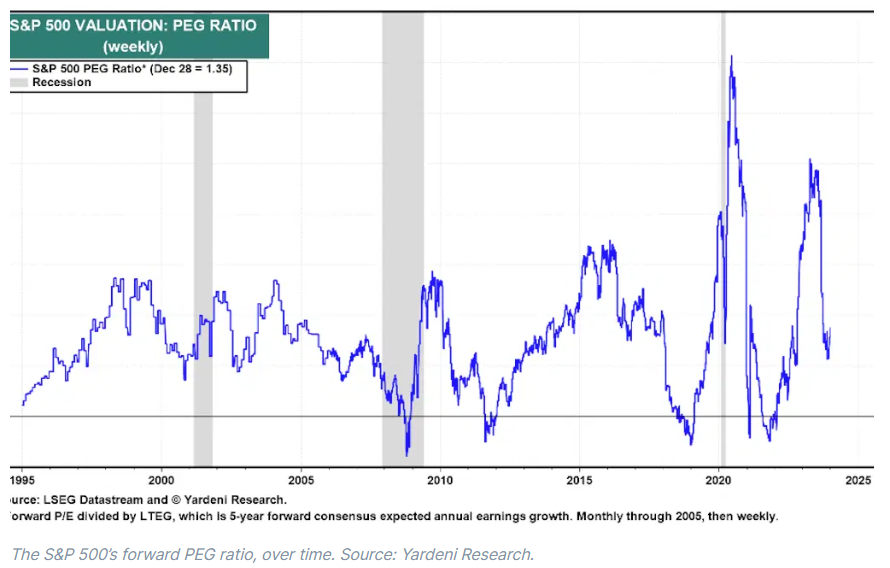

This next chart combines the S&P 500’s P/E ratio with its five-year average profit forecast. It’s called a PEG (price-to-earnings-to-growth) ratio and can be a handy way to quickly assess whether the P/E you’re paying for the index (or a stock) is worth the growth you might be getting. The lower the PEG ratio, the better the value.

Again, if analysts are right (and that’s a very big if) then the index wouldn’t seem to be excessively priced, at least, not compared to the past 30 years or so.

Or are you a bear?

If you answered no to three or more questions, you see a market that’s out over its skis. And you might’ve also noticed that my five questions are worded with a positive slant. That’s because I happen to fall on the bullish side – FWIW, I’m a big believer in the resiliency argument. But I have no problem with anyone who’d answer a flat-out no to all five questions. It’s perfectly plausible that inflation won’t creep lower, that global economies won’t avoid a recession, and – most importantly – that profit growth won’t keep up with the past. It’s also true that using PEG ratios to justify valuations can be dangerous. Think about it: there’s nothing worse than investing in something with a high valuation based on lofty growth expectations, only for that growth to disappoint. (In my defense, I only brought up the PEG to put the P/E ratio into perspective: I wouldn’t base an entire argument on it.)

And, finally, how to approach this market.

I don’t think anyone (including me) can argue that stocks are cheap. They’re not – the proof is there in the very first chart. The question, as always, is about what happens next and how to prepare your portfolio for it.

If you have a negative view of the future (for whatever reason) you’ll probably want to tread carefully, diversify across asset classes and regions, and focus on your long-term goals. Valuations can move around a lot, but what really matters over decades is profit growth, and there’s a decent chance that will still be decent.

If you have a more positive view of the future, you might think, as I do, that stocks aren’t cheap, but they’re not overly expensive either. (At least, not enough to get me selling.) Folks like us see the economic outlook as pretty good, and expect US companies to continue to churn out profit growth that’s close to the long-term average, if not better, assuming that AI works its magic and doesn’t destroy us all in the process.

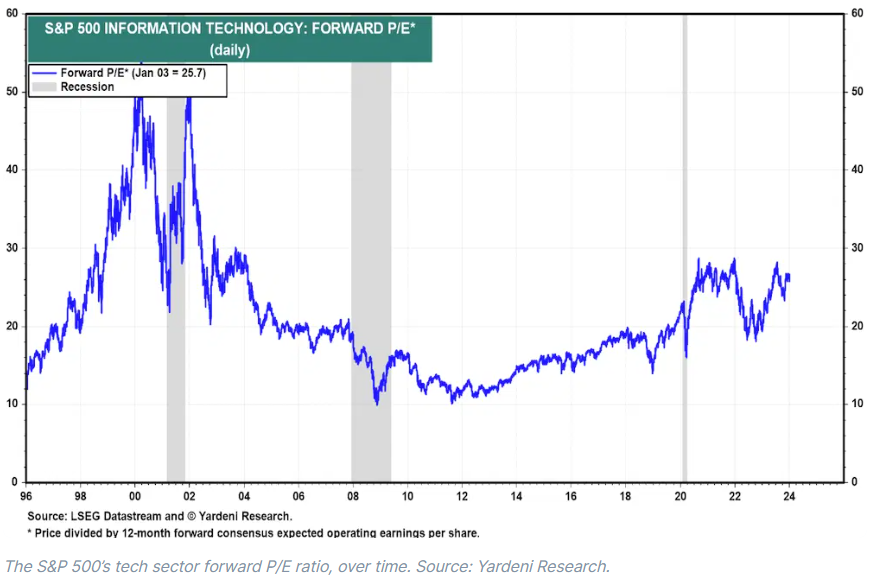

And, just for fun, let’s get really carried away for a second. If you’re a foam-at-the-mouth tech bull, it’s worth noting that the S&P 500 reached a record P/E of around 25x back in 1999 and the tech sector burst through 50x. Now, it’d be silly to start making predictions based on peak valuations, but AI (as regular investors know it) is barely a year old, and the internet spurred a bull market – and eventually a bubble – in tech stocks in 1999 that hasn’t yet been repeated. It’s an intriguing thought, if nothing else.

Paul Allison is a senior analyst at finimize

ii and finimize are both part of abrdn.

finimize is a newsletter, app and community providing investing insights for individual investors.

abrdn is a global investment company that helps customers plan, save and invest for their future.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.