Shares for the future: why I may rejig my scoring algorithm

Trade tariff volatility is affecting stocks in analyst Richard Beddard’s portfolio. In response, he’s considering changes to the way he scores them to help him beat the market over five-year periods.

25th April 2025 15:02

by Richard Beddard from interactive investor

This week, I’m interrupting the regular flow of company scores to pause for thought.

For background, I need to explain that you are reading this article about a week after it was written, and three weeks after the Trump administration’s Liberation Day tariffs.

- Our Services: SIPP Account | Stocks & Shares ISA | See all Investment Accounts

News coming thick and fast

I filed early because I am on holiday. In fact, I filed this article over a week ago, the day after I filed my previous article on Bunzl. I had to rewrite that article because the day I filed it, Bunzl (LSE:BNZL) dropped a profit warning.

Bunzl did not cite tariffs, just a more challenging economic backdrop - particularly in North America where it earns most of its revenue. Tariffs are surely contributing to the challenges businesses face there though.

Economic ructions expose weaknesses in companies we had not previously considered. Bunzl’s share price fell 25% that day.

The next company on my slate, promotional goods company 4imprint Group (LSE:FOUR), sources 60% of its revenue in China and earns 98% of it in the US. You would imagine tariffs could seriously raise costs.

4imprint’s annual report a year ago did not mention tariffs. The annual report published last week is sanguine about their direct impact. Like Bunzl, the knock-on effect on the US economy seems to be the bigger concern. But there is much uncertainty about whether tariffs will stick, and what those knock-on effects will be.

Last week I reduced 4imprint’s score by a point to reflect my uncertainty, but I delayed writing up the share. With news coming thick and fast, I feared I might have to interrupt my holiday to rewrite it.

Share Sleuth underperforming

Just as events can expose cracks in businesses, they can also expose cracks in investment strategies.

The sell-off in the Share Sleuth portfolio has been greater than the sell-off in the wider UK stock market as represented by the portfolio’s benchmark (accumulation units in a FTSE All-Share Index tracking fund).

- Stockwatch: is trade tariff risk really receding?

- Ian Cowie: four ways to tap into a potential trade war winner

Normally I would not worry about performance, everybody underperforms from time to time. But Share Sleuth has underperformed the tracker fund over the last five years.

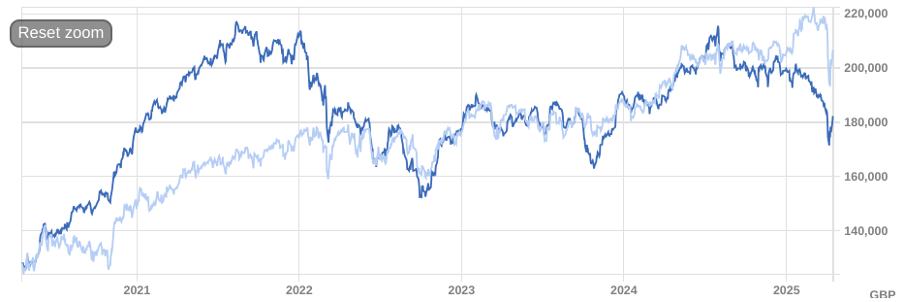

Data from ShareScope tells me that Share Sleuth was worth £128,202 on 16 April 2020. Today (the day I’m writing, not the day you are reading) is Thursday 17 April 2025 and at yesterday’s close it was worth £181,838, about 42% more. If I had invested the same amount in the tracker five years ago, it would be worth £206,469, an increase of 61%.

This is the chart, courtesy of ShareScope. The dark blue line is Share Sleuth. The light blue line is the tracker fund:

Past performance is not a guide to future performance.

One of my aspirations is to beat the tracker over five-year periods, so I need to think about whether I could be doing anything better.

My strategy is to assess whether a share is:

- Dependable (how reliably the company has performed in the past)

- Distinctive (which capabilities make the company special now)

- Directed (how well its strategy addresses the risks)

- Discounted (how the share price compares to average profit)

While this format is coherent, I have had niggling doubts about my execution. It’s a shame it took a major economic dislocation for these thoughts to begin to crystallise.

Raising the quality bar

The proximate issue I’m thinking about is the quality of the shares I’m scoring.

The Decision Engine contains 40 shares and the Share Sleuth portfolio, which draws from it, contains 26. This allows me to compare the scores of Share Sleuth holdings with shares that could take their place.

The first three criteria relate to the quality of a business. The Decision Engine is not suited to assessing companies that need to change radically. The goal is to identify businesses that have prospered and should continue to do well by building on strengths and adapting to challenges.

Businesses that need to change more radically will achieve lower scores, but these can hang around in the Decision Engine. There are two reasons for this. One is laziness (it is easier for me to rescore a share than to introduce a new one). Also, when it comes to jettisoning companies from the Decision Engine I focus on the lowest-ranked shares.

- Sector Screener: this food producer’s shares could keep growing

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

The lowest-quality businesses in the Decision Engine are not the lowest ranked of the 40 shares in the Decision Engine. The bottom seven shares are all companies I admire for different reasons. They are Bloomsbury Publishing (LSE:BMY), Garmin Ltd (NYSE:GRMN), Goodwin (LSE:GDWN), Cohort (LSE:CHRT), Tristel (LSE:TSTL), Celebrus Technologies (LSE:CLBS) and Keystone Law Group Ordinary Shares (LSE:KEYS). Their average quality score is nearly 8 out of a total of 9 (a maximum of 3 points for each criterion).

These are shares I would love to own in greater quantity, but their scores are weighed down because many traders fancy them too, and they cost high multiples of average profit. The Decision Engine is currently deducting an average of nearly 2 points from the scores of each of these shares because of their high prices.

Six of the shares immediately above them (ranked from 27 to 33) score 6 or less out of 9 for the quality criteria. The Decision Engine is adding an average of 1 point to the scores of each of these shares, because of their low prices.

Given the lower quality of these businesses, it is quite likely they need to make radical changes, or they are already making them and we are waiting to see the results.

At risk (quality score <6.5/9) | ||||||

Rank | Share | Description | Quality | Price | Total | Multiple |

27 | Sources, processes and develops flavours esp. for soft drinks | 6 | 1 | 7 | 6.7 | |

28 | Manufactures PEEK, a tough, light and easy to manipulate polymer | 6 | 1 | 7 | 7.1 | |

39 | Supplies software and services to the transport industry | 6 | 1 | 7 | 8.3 | |

30 | Manufactures natural animal feed additives | 6 | 0.9 | 6.9 | 12.5 | |

32 | Online retailer of domestic appliances and TVs | 6 | 0.7 | 6.7 | 14.3 | |

33 | Translates documents and localises software and content for businesses | 5.5 | 1 | 6.5 | 4.5 | |

Quality score is the combination of scores for Dependability, Distinctiveness and Direction

Price scores and profit multiples are determined by formulae in this explainer Date: Thursday 17 April 2025.

Since the Decision Engine is not suited to evaluating businesses needing or undergoing radical change, I think I need to find replacements for them.

I’m letting this idea sit with me while I am on holiday. If I feel the same way when I return, I will rejig the scoring algorithm, so the price score no longer promotes shares below a minimum quality threshold.

Then I will set about finding replacements for shares that fall below that threshold.

No shares for the future (this week)

I’m away this week and have not updated the Decision Engine table. Normal service will resume next week.

Macfarlane Group (LSE:MACF), 4imprint and Judges Scientific (LSE:JDG) have published annual reports and are due to be re-scored.

Richard Beddard is a freelance contributor and not a direct employee of interactive investor.

Richard owns many shares in the Decision Engine. He weights his portfolio so it owns bigger holdings in the higher scoring shares.

For more on the Decision Engine, please see Richard’s explainer.

Contact Richard Beddard by email: richard@beddard.net or on Twitter: @RichardBeddard

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.