Shares for the future: I think my final new stock is good value

As part of a spring clean, analyst Richard Beddard announces the last of the four new entrants in his Decision Engine, for now.

28th March 2025 15:04

by Richard Beddard from interactive investor

![Close-up of a person holding an orange [NEW] sign against a blue background](https://media-prod.ii.co.uk/s3fs-public/2025-03/newbutton_0.jpg)

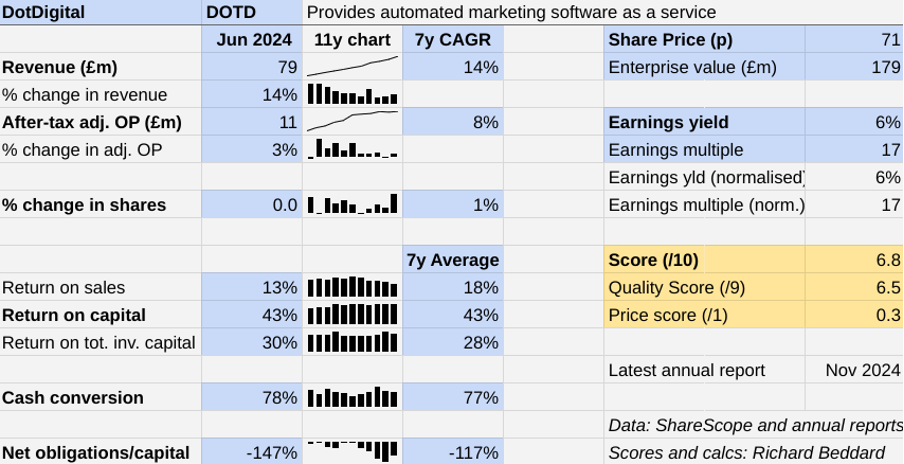

At first glance, dotDigital Group (LSE:DOTD) has a pristine track record. Over the past 11 years, the company has grown revenue at a 19% Compound Annual Growth Rate (CAGR) and adjusted profit has grown 12% (CAGR).

It has generated handsome quantities of cash and maintained a balance sheet untroubled by debt.

- Our Services: SIPP Account | Stocks & Shares ISA | See all Investment Accounts

Scoring DotDigital: Stalled profit growth

This decade, though, the marketing software platform’s profit growth has slowed.

The Past (dependable) [2.5]

- Profitable growth: Profit growth has stalled in real terms [0.5]

- Strong finances: Net cash [1]

- Through thick and thin: Lowest return on capital 35% (2014) [1]

Over the past four years, revenue growth of 14% CAGR has been somewhat lower, and adjusted profit growth of 3% CAGR has been much lower than the 11-year growth. These numbers compare even less favourably to the decade before 2020.

In the year to June 2024, Dotdigital’s performance was typical of this lower-growth period. This is a conundrum because the company believes the pandemic accelerated interest in digital marketing.

In February, Dotdigital said it expected to achieve analysts’ forecast for the full year to June 2025. That being the case, we can expect a 9% increase in revenue to £86.2 million and an 8% increase in company adjusted profit (before tax) to £18.1 million.

It would not be a bad performance, but still not what shareholders a decade ago were experiencing.

The Present (distinctive) [2]

- Discernible business: Marketing software as a service [0.5]

- With experienced people: Experienced CEO, founder owns 10% [1]

- That creates value for customers: All-in-one marketing platform [0.5]

Dotdigital is a cloud-based marketing automation software platform. At its heart is a database that consolidates the information an organisation has gathered about its customers.

Dotdigital’s software tells organisations about their customers or other constituencies, and allows them to divide people into segments with similar attributes.

Marketeers use the Dotdigital interface to create, send and test automated and personalised messages. They are sent through email, SMS, chat, mobile apps and websites.

About half Dotdigital’s customers are commerce customers, where a purchase is the end goal. They include EDF, Krispy Kreme, Specsavers and Volvo.

The other half of Dotdigital’s customer base includes businesses, public sector bodies such as the NHS and local councils, and charities that communicate with employees, constituents and donors.

Dotdigital’s original product was dotmailer, which focused on email, but the acquisition of Comapi in 2017 brought SMS capabilities. In 2023, it acquired Fresh Relevance, and the capability to personalise web pages. The company has invested to integrate these capabilities and develop others.

I think platform expansion explains why costs have increased as a proportion of revenue. In particular, my suspicion falls on one line in the company’s cost of sales: “Outsourcing and Tech Infrastructure”.

Outsourcing and tech infrastructure includes SMS messaging, which is routed over mobile networks at a cost to Dotdigital. The company says SMS earns a gross profit margin of less than 50% compared to about 90% for email.

The Dotdigital platform is also hosted on major cloud service providers, principally Microsoft Azure and Amazon Web Services. It uses ChatGPT to help marketers create their messages.

The cost of outsourcing and tech infrastructure was 20% of total revenue in 2024, compared to 8% in 2020. It was probably much lower in the middle of the last decade when Dotdigital was focused on email and had yet to migrate to the cloud service providers.

As the platform has grown in complexity, Dotdigital has also spent more to develop it. Capitalised development costs have increased from about 8% to about 13% of total revenue since 2016.

It may also be that international growth has acted as a brake on profit growth, due to the cost of establishing Dotdigital in new markets. In 2016, Dotdigital earned about 18% of total revenue overseas, compared to 32% in 2024. Its most immature market is Japan where it is earning annualised recurring revenue of about £1 million after two years.

Overseeing the expansion of the platform and where it is sold, has been chief executive Milan Patel, who joined Dotdigital in 2007 and became chief executive in 2016 (after a brief stint as chief financial officer). The company’s chief financial officer is standing down in April after less than three years.

Founder and president Tink Taylor is a digital marketing luminary, but he no longer sits on the board. He owns a 10% stake.

The Future (directed) [2]

- Addressing challenges:Dependence on partnerships, Competition [0.5]

- With coherent actions: New partnerships, innovation, acquisitions, geographical expansion [0.5]

- That reward all stakeholders fairly: Customer, employee focused [1]

I think Dotdigital’s expansion has caused its contraction in profit growth. That is not to blame the strategy. The company would be much smaller had it not embraced the proliferation of marketing channels or moved outside its UK heartland.

During a half-year results presentation in February, Dotdigital said one of its latest additions, the web personalisation platform Fresh Relevance, was not only adding new revenue, it was helping the company retain revenue.

The web personalisation capability prevented a sizable customer, generating £13,000 of revenue per month, from switching to a rival that already offered it.

It seems that addressing a proliferation of marketing channels is required to compete, and one thing that has always worried me about marketing platforms is that there is a bewildering array of competitors.

Whether Dotdigital has to build, partner or buy its way to being an all-in-one platform, the company is committed, which is probably why it now describes itself as a Customer Experience and Data Platform (CXDP).

Milan Patel says the next logical step in its evolution is search and merchandising. Dotdigital wants to use its data platform to personalise customer website search results based on customers’ behaviour and previous purchases. It is also working on a loyalty platform.

The acquisition of Fresh Relevance might, therefore, be a catalyst for more lucrative non-SMS revenues that make more use of the data Dotdigital warehouses. The two platforms have blended interfaces so they work well together, but retain separate branding.

More acquisitions are mooted, but Dotdigital says valuations in private markets are higher than in public markets, so they are hard to come by at a reasonable price.

The company continues to develop the platform. It is already integrated with Google Ads and Facebook and recently introduced integrations enabling targeted advertising in TikTok and LinkedIn.

A WhatsApp integration to be launched next month is almost exclusive, for now. Meta, WhatsApp’s parent, is testing the water with two providers: Dotdigital and Braze.

Dotdigital has also been working on in-app push notifications. These are messages sent by Dotdigital that appear in customers’ mobile apps in response to their activity.

The third element of Dotdigital’s strategy is to integrate with other software systems, principally e-commerce software such as Adobe and Shopify, and Customer Relationship Management (CRM) and Enterprise Resource Planning (ERP) systems.

Dotdigital already supports 190 technology integrations that it says address 70% of medium-sized companies, its sweet spot. A newish partnership with Oracle Netsuite, could, Dotdigital says, become a strategic partnership worth more than 10% of revenue.

The company says it is focused on employee career development and managing a healthy level of employee churn, but it does not divulge figures. Its customer satisfaction score, derived from over 1,000 customer ratings a month following interaction with the support team, is 99%. Dotdigital says this is world class.

The price (discounted?) [0.3]

- Yes. A share price of 71p values the enterprise at about £179 million, 17 times normalised profit.

A score of 6.8 implies Dotdigital may be a good long-term investment.

It is ranked 29 out of 40 shares in my Decision Engine.

While Dotdigital is only on the cusp of good value, I think the Decision Engine will be improved if I include it and remove PZ Cussons (LSE:PZC), which has a score of 4.4 and is ranked 40.

I have made the switch.

27 Shares for the future

Here is the ranked list of Decision Engine shares. I review the scores at least once a year, soon after each company has published its annual report. The price scores are calculated using the share price prior to publication.

Generally, I consider shares that score 7 or more out of 10 to be good value. Shares that score 5 or 6 out of 10 are probably fairly priced.

Bunzl (LSE:BNZL), Howden Joinery Group (LSE:HWDN) and Quartix Technologies (LSE:QTX) have all published annual reports and are due to be re-scored.

0 | company | * | description | score |

1 | Manufactures tableware for restaurants and eateries | 10.0 | ||

2 | Supplies kitchens to small builders | 9.3 | ||

3 | Imports and distributes timber and timber products | 9.0 | ||

4 | Makes light fittings for commercial and public buildings, roads, and tunnels | 8.9 | ||

5 | Manufactures pushbuttons and other components for lifts and ATMs | 8.5 | ||

6 | Distributor of protective packaging | 8.4 | ||

7 | Repair and maintenance of rail, road, water, nuclear infrastructure | 8.2 | ||

8 | Manufacturer of scientific equipment for industry and academia | 8.2 | ||

9 | Whiz bang manufacturer of automated machine tools and robots | 8.2 | ||

10 | Manufactures computers, battery packs, radios. Distributes components | 8.1 | ||

11 | Flies holidaymakers to Europe, sells package holidays | 8.1 | ||

12 | Manufactures filters and laboratory equipment | 8.1 | ||

13 | Sells promotional materials like branded mugs and tee shirts direct | 8.0 | ||

14 | Designs recording equipment, loudspeakers, and instruments for musicians | 8.0 | ||

15 | Distributes essential everyday items consumed by organisations | 7.9 | ||

16 | Manufactures vinyl flooring for commercial and public spaces | 7.7 | ||

17 | Surveys and distributes public opinion online | 7.7 | ||

18 | Manufactures surgical adhesives, sutures, fixation devices and dressings | 7.6 | ||

19 | Operates tenpin bowling and indoor crazy golf centres | 7.6 | ||

20 | Retailer of furniture and homewares | 7.6 | ||

21 | Manufactures/retails Warhammer models, licences stories/characters | 7.4 | ||

22 | Online marketplace for motor vehicles | 7.3 | ||

23 | Sells hardware and software to businesses and the public sector | 7.3 | ||

24 | Manufacturer of ventilation products | 7.1 | ||

25 | Manufactures PEEK, a tough, light and easy to manipulate polymer | 7.0 | ||

26 | Supplies software and services to the transport industry | 7.0 | ||

27 | Sources, processes and develops flavours esp. for soft drinks | 7.0 | ||

28 | Manufactures natural animal feed additives | 6.9 | ||

29 | DotDigital | Provides automated marketing software as a service | 6.8 | |

30 | Online retailer of domestic appliances and TVs | 6.7 | ||

31 | Acquires and operates small scientific instrument manufacturers | 6.6 | ||

32 | Translates documents and localises software and content for businesses | 6.5 | ||

33 | Publishes books, and digital collections for academics and professionals | 6.2 | ||

34 | Casts and machines steel. Processes minerals for casting jewellery, tyres | 6.0 | ||

35 | Manufactures disinfectants for simple medical instruments and surfaces | 5.9 | ||

36 | Manufactures military technology, does research and consultancy | 5.9 | ||

37 | Supplies vehicle tracking systems to small fleets and insurers | 5.7 | ||

38 | Manufactures sports watches and instrumentation | 5.6 | ||

39 | Makes marketing and fraud prevention software, sells it as a service | 5.6 | ||

40 | Runs a network of self-employed lawyers | 4.8 |

Scores and stats: Richard Beddard. Data: ShareScope and annual reports

Click on a share's name to see a breakdown of the score (scores may have changed due to movements in share price)

Shares marked with an asterisk (*) have been re-scored, click the asterisk to find out why.

Richard Beddard is a freelance contributor and not a direct employee of interactive investor.

Richard holds many shares in the Decision Engine. He weights his portfolio so it owns bigger holdings in the higher-scoring shares.

For more on the Decision Engine, please see Richard’s explainer.

Contact Richard Beddard by email: richard@beddard.net or on Twitter: @RichardBeddard

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.

AIM stocks tend to be volatile high-risk/high-reward investments and are intended for people with an appropriate degree of equity trading knowledge and experience.