Share of the week: A dividend payer?

10th February 2017 16:44

by Harriet Mann from interactive investor

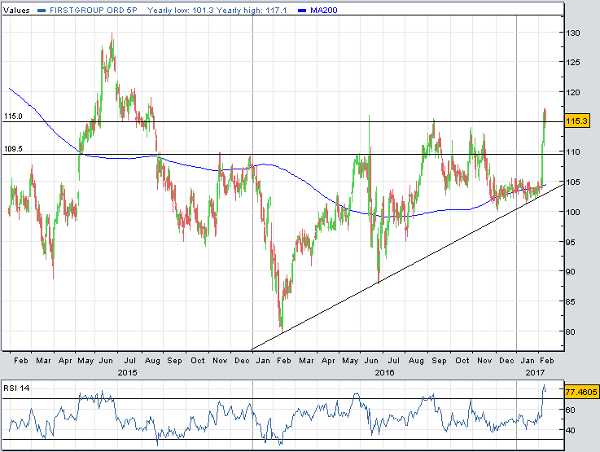

This time last year, British transport company was hurtling towards an all-time low, as terrible weather and flooding forced the group to lower its profits guidance after a tricky few years. Filling the gap, the shares then clawed themselves back to 110p, before slumping again in a post-referendum sell-off.

Dancing on hot coals, the shares have jumped between 79p and 116p throughout the last year, pausing for breath in two months of rare stagnation over December and January.

But this week's third-quarter trading statement propelled the shares back up to an 18-month high at 117p. Up 12%, FirstGroup is a FTSE 350 top performer and our share of the week.

FirstGroup has had a tough time over in recent years. The government stripped the business of its West Coast rail franchise after uncovering issues with the bidding process in 2012. The firm was subsequently forced to axe its dividend and launch an emergency £615 million rights issue.

It's struggled to kick-start a turnaround since, but has said it hopes to generate a lot more cash this year, which has investors crossing their fingers for a restoration of its dividend.

Currency tailwinds underpinned a 12.8% jump in group revenue in the third quarter, with turnover flat at constant currency. Changes to rail franchises and issues at First Bus offset growth in North America. A focus on pricing in the First Student business saw sales inch 1% higher in the three months, while growth in its Transit division was accelerated by both new and existing business.

With Prime Minister Theresa May on course to trigger Article 50 before the end of March, the outlook here is uncertain. There are already challenges weighing on the bus business and promising rail operations were weighed down by a slowdown from GWR and engineering works.

With management maintaining full-year forecasts, broker UBS has done the same. Analyst Peter Larkin reckons revenue will jump 9% to £5.7 billion this year, with operating profit up 8% to £325 million, giving earnings per share of 11.85p.

He's also confident a return of the dividend could be on the cards. If FirstGroup pays out a 4.6p (re)maiden dividend, the shares are currently yielding 4%.

This recovery story is still just finding its legs, however. With plenty of hurdles ahead, Larkin has kept onto his 108p target price and 'neutral' rating for now.

This article is for information and discussion purposes only and does not form a recommendation to invest or otherwise. The value of an investment may fall. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.