More than a third of investors oppose ‘wealth tax’

interactive investor comments on Wealth Tax Commission report.

10th December 2020 11:24

by Rebecca O'Connor from interactive investor

interactive investor comments on Wealth Tax Commission report.

This week’s Wealth Tax Commission report, which proposed the UK introduce a wealth tax, was never going to be universally welcomed.

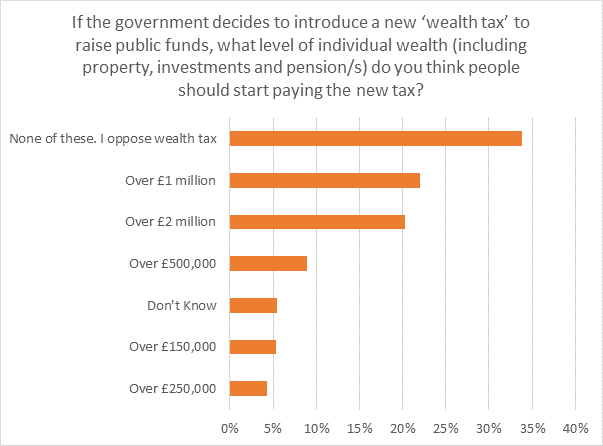

A recent poll by interactive investor ahead of last month’s spending review found that 34 % of investors were opposed to a wealth tax; 22% supported a threshold of £1 million, while 20 per cent said the threshold should be £2 million.

Only 14% said £500,000 should be threshold – the level suggested by the Wealth Tax Commission report.

Becky O’Connor, Head of Pensions and Savings at interactive investor, said: “They might not know it, but most Brits already pay a wealth tax on their investments, with many investment platforms (a rare exception being flat fee provider interactive investor), charging a percentage fee.

“Percentage fees mean that as your wealth grows, you pay more in charges. With the Government looking increasingly likely to get in on the action, investors need to start looking at how they can keep as much of their own money as possible. You can’t control what the Government does, but you can control the charges you pay.

“The introduction of a wealth tax would have to be sensitive to the inability to pay of many ‘asset rich, cash poor’, who may be older and unable to work or actually access any of their wealth.

“It would also have to carefully balance the need to continue incentivising long-term investing, through pensions and ISAs, which contributes to economic growth, with the need for additional government revenue.

“There would be further practical issues, such as the difficulty of the valuation of assets like defined benefit pensions.

“There are also concerns that such a tax would still not be paid on the ultra-wealthy, but would be shouldered by ‘mass affluent’ older people, with family-sized homes and their mortgages paid off, as well as large pension pots accumulated through working life.

“It’s also important to bear in mind that while a defined contribution pension worth £500,000 might sound like a lot on paper, it has to last someone potentially 20 years or longer after they give up work.

“Currently, a pot worth £500,000 would buy an annuity income for life of around £18,000 a year.

“The potential need for people to pay for long-term care in later life is another significant drain on pension and property wealth.”

In its Great British Retirement Survey, interactive investor found that the biggest concern among non-retired people (27%) is that money they would like to leave to children will go on long-term care, meanwhile the biggest fear among retired people (22%) is “not being able to leave loved ones money when I die”.

The survey also found that people in and approaching retirement were using their pensions to help adult children with property deposits.

More than half (51%) of retired respondents had helped their children buy property and one-in-five non-retired respondents with children who had taken a lump sum had used it to help the younger generation, putting their own retirement income potentially at risk to do so.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.