Microsoft could become a $5 trillion dollar firm

9th June 2023 14:01

by Paul Allison from Finimize

I’ve taken a completely different approach to thinking just how big Microsoft could get. And the conclusion is eye-opening.

Based on a reverse discounted cash flow, investors are expecting Microsoft Corp (NASDAQ:MSFT) to post roughly 10% cash flow growth for the next ten years, and 2.5% thereafter.

That seems pretty reasonable considering 1) the firm has delivered 10% growth on average over the past ten years 2) IT spending as a percentage of the economy and Microsoft’s share look set to increase, and 3) Microsoft has an opportunity to capture – through higher prices – AI’s massive productivity savings.

Whatever Microsoft’s potential (or lack thereof) may be, this sense check would suggest the stock isn’t in bubble territory – at least not yet.

As one of the AI elites, Microsoft has seen its shares skyrocket this year, leaving investors wondering whether they’re overvalued at this point. With any valuation assessment, it’s a good idea to start with what you think the market is pricing in. From there it’s about thinking through whether that seems unrealistic or not. I’ve used my trusty valuation framework to do that, and deployed two angles of attack to help you decide whether you think that’s unrealistic or not. Then – just for fun – I’ve taken a completely different approach to thinking just how big Microsoft could get. And the conclusion is eye-opening, to say the least.

What kind of growth rate is already priced in?

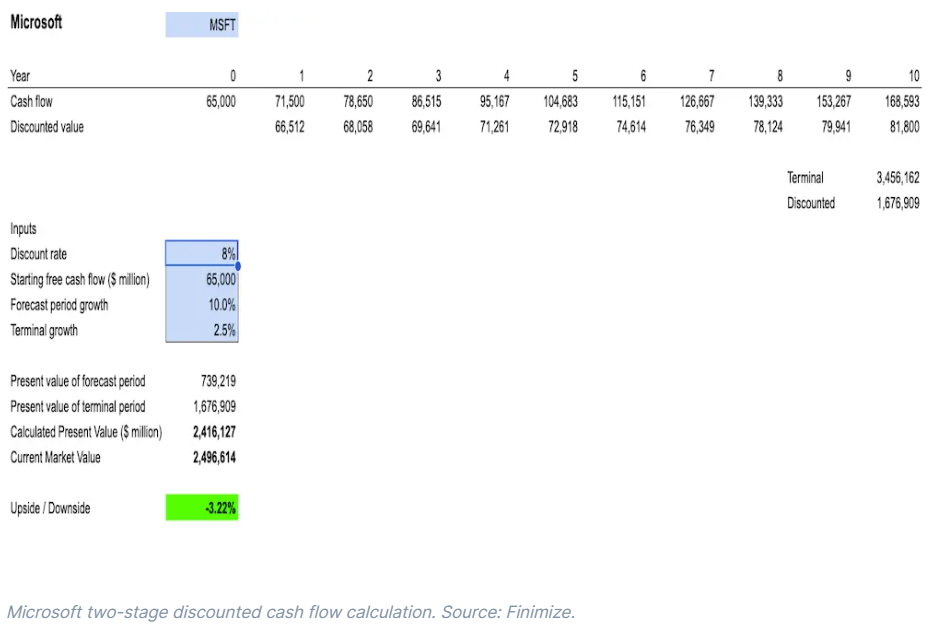

A quick glance at Microsoft’s price-to-earnings (P/E) valuation is a tad concerning – at a 32x multiple, it’s pretty near its 20-year high from 2021. But P/E ratios that use past or near-term profit forecasts aren’t that useful in valuing growth firms like Microsoft. The company’s uber-profitable already, sure, but, still, most of its profit will come well into the future. So the best way to get your arms around what’s baked into MSFT’s current stock price, then, is to conduct a relatively straightforward reverse two-stage discounted cash flow (DCF) analysis.

A conventional DCF forecasts a firm’s cash flow for a set number of years (usually ten), then assumes a forever growth rate after that – normally a rate in line with economic growth (say, 2.5%). It then discounts all those cash flows using an interest rate back to today’s value and adds them up to get a firm valuation.

A reverse DCF, on the other hand, involves playing around with those growth numbers until you get a valuation that matches today's market valuation and is a helpful way to see what the market is actually assuming now. And as your good luck would have it, I wrote all about reverse DCFs in this article, which includes a downloadable template that you can use.

Using last year’s cash flow as our jumping-off point, and a 7.5% discount rate, you can see that the market is assuming roughly 10% growth in cash flow for the next ten years for Microsoft, and an economic-growth-like 2.5% expansion after that. But that doesn’t tell you enough in isolation, so you’ll want to contextualize that 10% growth rate, and ask yourself, “Is this reasonable?” Here are a couple of quick ways to do that…

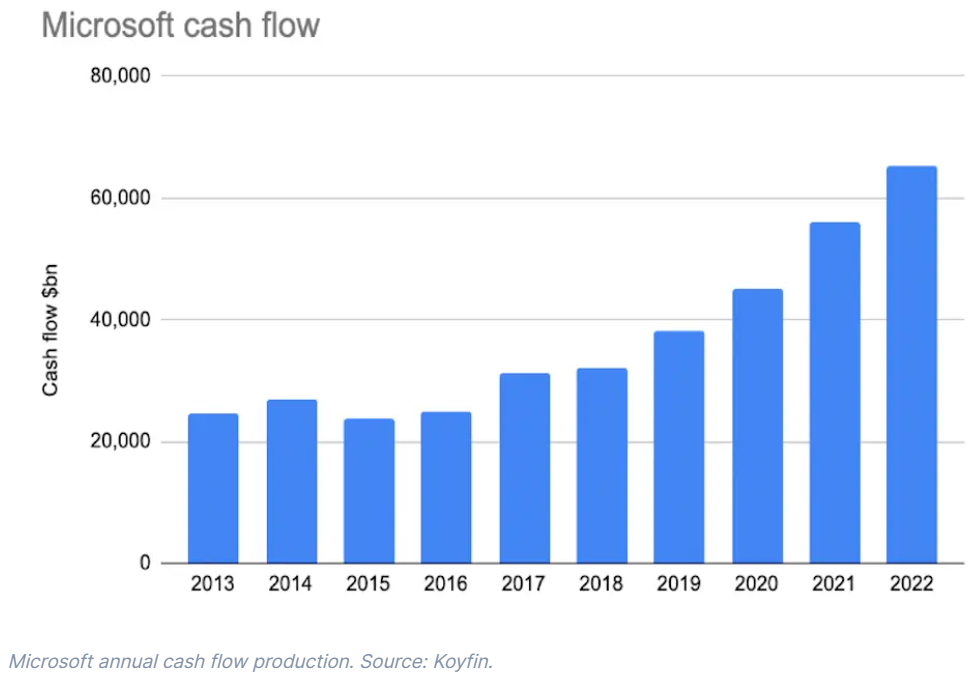

1. Look back over the past ten years.

It’s been an impressive decade for Microsoft, especially the latter half of it when cloud computing really took off. This chart shows the expansion in cash flow since 2013.

Microsoft’s cash flow has leaped some $40 billion since 2013, which works out to be an average of just over 10% a year. That’s a pretty decent performance – it’s also (conveniently) bang in line with our reverse DCF calculation above.

The question, then, becomes: will Microsoft’s AI future be as good as its cloud-driven past? If you’re an AI super-bull (and there are plenty out there), you probably think that 10% future growth in cash flow massively undercooks Microsoft’s potential. But if you’re a skeptic, you might think Microsoft will underperform its recent past. My view is that, with cloud and AI both driving revenue, it’s credible to believe Microsoft’s future growth could at least match its past. And that suggests the current stock price isn’t unrealistic.

2. Estimate the size of the total addressable market.

The global economy is currently pegged at around $100 trillion, and according to technology data firm Gartner, global IT spend is close to 5% of that, at $4.5 trillion. Now, Microsoft CEO Satya Nadella said back in 2020 – that’s before all this AI buzz kicked off – that tech spending as a percentage of the global economy is set to double over the next ten years. So let’s just assume for a moment that he’s right. If the global economy grows at 2.5% for ten years, it’ll be worth around $128 trillion in 2033. And if IT spending were to roughly double to 10%, it’d be a whopping $12.8 trillion of that.

Now, with sales of around $220 billion – that’s a rough estimate for this fiscal year, which ends in June – Microsoft commands around 5% of current global IT spend. So let’s say the firm simply holds its current share and gains no more. That’d equate to sales of $640 billion ten years from now – 190% higher than current levels and, at 11% a year, is magically close to the 10% a year that’s currently “priced in”.

But there’s also the possibility that Microsoft’s share of global IT spending will grow – the firm’s bosses would make a strong case for that, anyway. So let’s say it does creep up to a not-inconceivable 6%. That’d yield sales of around $770 billion: an annual growth of 13%. Keep in mind that we’re talking sales here and not cash flow (which we used in our DCF and historical comparison). Through cost discipline, Microsoft would hope to grow profit and cash flow faster than sales – so maybe those would rise at 15%, or 18%.

This type of analysis is known as total addressable market – or TAM – and requires a lot of educated guessing. But that’s fine. Remember we’re not trying to be hyper-precise here, we’re essentially “sense checking” the 10% growth rate assumption that’s baked into Microsoft's share price. And what these numbers tell me is that there’s no evidence of a bubble-like valuation in Microsoft’s shares.

3. Then – because, why not? – take a stab at just how big Microsoft could get.

There’s another, more “bottom-up” way to think about the problem, and that’s to piece together the potential for Microsoft’s products. There are currently around 350 million users of Microsoft’s commercial (that’s work-related) office products. If you assume that the commercial office business makes up around 40% of Microsoft’s total sales of $220 billion, it works out at revenue of around $1 per working day per commercial office user (using 260 working days). Now, the average knowledge worker in the US earns around $40 an hour. If Microsoft’s now generative AI-infused software saves workers as much time as the firm’s bosses say it will, then it’s not a stretch to think that all knowledge workers might get back a couple of hours every working day – that’s $80 per worker per day saved.

Of course, that’s not money in any firm’s pocket until it reallocates that $80 in other money-making activities, or uses AI to replace costly workers. But it’s a potential productivity savings all the same. The question, then, is: how much of that $80 could Microsoft keep by raising prices on its AI-loaded, cost-saving software? Just for fun, let’s say Microsoft keeps $5. That would mean $6 per Microsoft user per day, which would equate to $546 billion a year – more than twice Microsoft’s total current revenue. That’s a big number and we haven’t even accounted for Azure – Microsoft’s rapidly growing, $100 billion cloud business – or indeed its consumer segment, which includes gaming. Throw those into the mix and MSFT’s revenue could be closing in on $1 trillion in ten years. Now, what value you place on that is up to you, and it’d depend on what the following ten years looked like (that’s years 2033-43). But currently, Microsoft trades on 10 times sales. Half that valuation still leaves a $5 trillion company.

That’s food for thought.

So, what’s the bottom line?

Look, it can be easy to be blinded by dollar signs, so try to remember that there are still loads of risks to all these assumptions. Microsoft, by its own admission, hasn’t figured all of this out yet: it’s still getting its arms around just how useful its AI-infused products might be for customers. And it’s perfectly plausible that workers don’t take to the new way of doing things, or that they take longer than expected to adopt the new technology – no one likes change and all that. Perhaps the biggest risk (and it’s not a pleasant thought) is that AI experiences some kind of dangerous breakout moment in the next few years, which could prompt a complete rethink of the technology’s entire use case. If that were to happen, there’d be some very serious concerns cast over all those AI-elite stocks.

But the point of this exercise has been to “sense check” current investor expectations, using a few different lenses to see whether there’s evidence of a bubble (with some more imaginative scenarios thrown in). Usually, when bubbles exist, and you do these exercises, you find yourself having to push your growth numbers to unrealistic levels – or worse, lower your discount rate – to justify a stock price. And that should leave you in a state of disbelief. But that’s not been the case here with Microsoft. That 10% growth rate seems perfectly plausible, which can only leave one conclusion: no bubble, at least not yet.

Paul Allison is a senior analyst at finimize

ii and finimize are both part of abrdn.

finimize is a newsletter, app and community providing investing insights for individual investors.

abrdn is a global investment company that helps customers plan, save and invest for their future.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.