Is it (finally) a small-caps world after all?

A look at the what, why, how, and when in the US small-cap space and what's to come in 2025.

26th February 2025 12:13

As investors seek assets that will shine under a second Donald Trump presidency, one corner of the US stock market expects to benefit.

With Donald Trump securing his second term, uncertainty around election results has been replaced with America-first policies. We believe these policies, which signal a greater focus on domestic growth, are poised to benefit US small-cap stocks in several ways, particularly given their current significant discount compared to their larger counterparts.

Despite the relative outperformance of large caps in 2024, US small caps delivered strong absolute returns, with the Russell 2000 gaining over 11%. Encouragingly, our US small-cap strategy outperformed significantly, achieving a gross return of approximately 5.7% above the benchmark.

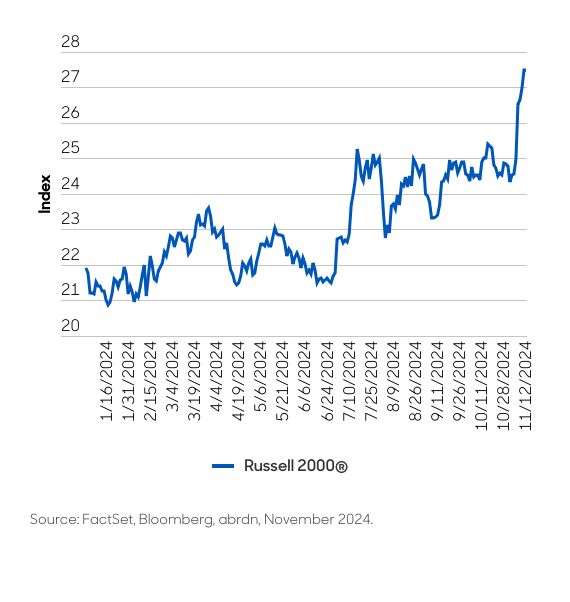

The small-cap index saw a sharp spike following the election result. The Russell 2000 Index closed 5% higher (Chart 1) as it became clear Trump had won and rose by 20% the week after, possibly signaling an upswing in sentiment among small-cap investors. (1)

Chart 1. Russell 2000’s post-election surge

With the momentum in consumer sentiment and shifts – both current and potential – in political policies, we believe the stage is set for several key trends that could shape the trajectory of US small caps in 2025:

What? Smaller US companies with increasing profit and cash flow profiles.

Why? Trading with attractive valuation disparity to large-cap stocks relative to history and offering diversification benefits away from US large-cap stocks, with several potential tailwinds.

How? A quality-focused investment process drives a concentrated portfolio with a longer-term view, blending informed macroeconomic considerations with active, bottom-up, fundamental research.

When? Historical data suggests holding for the long term gives the best results. However, current valuations, rate cuts, and a pick-up in mergers and acquisitions (M&A) activity indicate that now may be a good time to allocate to the asset class.

Setting up for the next small-cap decade?

Small caps have historically traded at a premium to large caps. Since the Global Financial Crisis, strong performance from US large caps has helped drive large-cap valuations to one of their largest premiums over small caps in history. The cycles of large-cap vs. small-cap relative performance tend to be long, and we may be near the start of a change in that cycle (Chart 2).

Chart 2. Cyclical trends for the small-cap asset class are favorable (1931–2024)

Diversification benefits

A meaningful allocation to small caps offers significant diversification benefits. Due to their revenue sources and sector allocations, small caps give investors access to different risk characteristics compared to large-cap stocks. Additionally, small caps tend to be more domestically focused than larger peers and often operate in the most dynamic areas of the US market.

A long-term and strategic allocation

Given the clear performance and diversification benefits, we believe an allocation to the asset class should be long-term and strategic. With the outperformance of US large caps over the past decade and a half, it may be hard to see the benefits of investing in smaller companies. However, we believe several factors suggest that now may be an attractive time to allocate.

Attractive valuation disparity

US small caps are trading at a generational discount to their large-cap peers on a relative basis. Small caps have historically traded at a premium to large caps (Chart 3), but the recent long cycle of large cap outperformance has left small caps at a substantial discount.

Chart 3. Small cap relative to large cap forward price/earnings (PE) ratio

This disparity presents a unique opportunity for investors to buy into small caps at attractive prices.

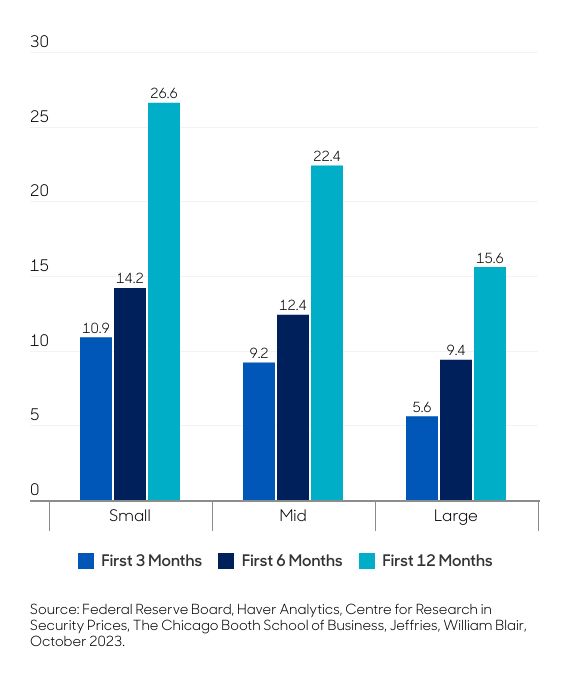

Rate cut timing

Historical data (since the 1950s) shows that smaller companies have outperformed larger peers following the first rate cut, and the current economic environment may support this trend (Chart 4).

Chart 4. Small cap vs. mid and large cap after first rate cut

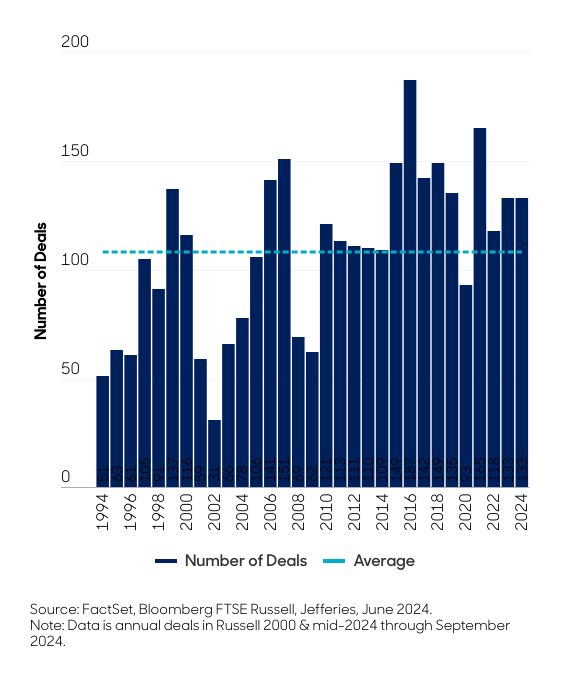

M&A likely to continue

Growth and scale are crucial in today’s climate, while corporate balance sheets are also flush with cash (around $2.6 trillion). This should trigger a flurry of M&A activity. Previously, small-cap companies benefitted from increased M&A activity, as they are often seen as attractive acquisition targets by larger firms and private equity investors. The relative undervaluation and strong performance of small caps indicate an uptick in M&A activity across the asset class (Chart 5). Historically, small caps rise by nearly 16% when M&A activity accelerates, a trend we are beginning to see in 2025.

Chart 5. M&A activity accelerating in small caps

Trump's policies, which aim to stimulate economic growth and increase corporate profitability, can further drive M&A activity, providing additional support for small-cap valuations.

Structural advantages in a higher interest rate environment

As we highlighted, interest rates are expected to gradually decline over time. However, they remain significantly higher than pre-pandemic levels. Additionally, the prospect of Trump’s looser fiscal policies and potential supply-side shocks further raise inflation expectations. This could prevent the US Federal Reserve from cutting rates further. However, such a situation creates structural advantages for higher-quality companies, which are better equipped to manage elevated interest rates than their lower-quality counterparts.

A core tenet of the investment strategy is to focus on high-quality small-cap companies, positioning the strategy well to capitalize on this trend.

Final thoughts

Investing in US small caps offers a compelling opportunity for diversification and potential long-term gains. The attractive valuation disparity, potential tailwinds from rate cuts and M&A activity, and the benefits of a quality-focused investment process make small caps an appealing addition to an investment portfolio. While the recent outperformance of large caps may overshadow the immediate benefits of small cap investing, we believe the long-term potential remains strong. Investors can capitalize on this unique opportunity by taking a strategic, long-term approach and focusing on high-quality companies.

Christopher Colarik is small-cap portfolio manager at abrdn.

Tom Harvey is senior equity specialist at abrdn.

ii is an abrdn business.

abrdn is a global investment company that helps customers plan, save and invest for their future.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.