How to prepare your portfolio for the new era of spikeflation

13th June 2023 11:00

by Ceri Jones from interactive investor

Some fund managers think high inflation isn’t over and that investors should brace for a new regime of ‘spikeflation’. Ceri Jones considers how investors should prepare for such a scenario, and names investments that could provide resilience.

UK inflation is proving stubborn, and is likely to remain high and volatile throughout the winter and beyond. The latest figure for UK inflation was 8.7% in April, which although a drop from 10.1% in March, is still much stickier than in the US, where the headline rate is around 4.9%.

Much of this disparity is down to energy prices, because Western Europe has traditionally relied on Russia for 40% of its gas, while the US has successfully reinvigorated its shale gas industry. Furthermore, the UK is at a disadvantage in being able to store only 1% of its annual gas requirements, compared for example with around 25% in the rest of Europe. UK inflation could therefore continue to spike if energy price inflation is exacerbated by a cold winter.

- Invest with ii: Buy Global Funds | Top Investment Funds | Open a Trading Account

Inflation might also be exacerbated in the coming months by a number of additional macro shocks, says Trevor Greetham, head of multi-asset at Royal London Asset Management, who predicts ‘spikeflation’, periods of spikes in inflation in the years ahead, as prices rise in response to these events.

As well as further energy price rises over the winter, Greetham says potential setbacks include “the path to net zero, which reduces fossil fuel supply, a very uncertain geopolitical backdrop and a process of deglobalisation. Populism and high government debt levels also create an incentive for governments to let inflation run hot,” he says.

Jury out on the 60/40 portfolio model

In this inflationary environment, few investment managers now believe a traditional 60/40 portfolio is sufficiently diversified, preferring to add liquid alternatives such as commodities, commercial property and listed renewables, as well as stores of value such as gold and the Swiss franc.

“Both stocks and bonds fell over 2022, and both asset classes posted negative real returns in other inflationary periods, such as the 1970s, late 1980s and 1994,” says Greetham.

“We prefer a broadly diversified mix including commodities, commercial property and a higher allocation to UK equities than suggested by market capitalisations, as the UK market is particularly resilient to inflation, by dint of its lower valuation and sector mix tilted towards energy and resource sectors.

“Spikes in inflation tend to mean shorter business cycles, as central banks slam on the brakes more often, and more frequent bear markets, requiring an active approach to tactical asset allocation.”

- Should you invest in Baillie Gifford funds or investment trusts?

- The shares fund managers regret not selling sooner, and lessons learned

- Why there’s plenty of life in these dinosaur stocks

Ian Samson, portfolio manager, multi asset, at Fidelity International, points out that historically inflation has proved hard to tame.

He thinks there “is a material risk that we enter a period of high, or at least more volatile, inflation. This was the case from the early 1970s until the late 1990s.”

Samson notes this has huge implications for multi-asset funds, and by extension DIY investors building their own diversified portfolios.

He continues: “Most importantly, in a world of inflation fears, government bonds will be positively correlated with risky assets.

“This makes 'duration' a very poor hedge for portfolios, while still underperforming in bull markets. Indeed, from the 1970s through the 1990s, a 50/50 equity/cash portfolio had a meaningfully better risk-reward than 50/50 equity/bonds.”

Be on the lookout for opportunities

Critically, however, at a period when most of the investment industry appear to be running scared, brave investors can often find a good entry point.

“When clients and market commentators all say the same thing, then the biggest risk in this environment is to get too close to the headlines, and not look for opportunities,” says Matt Bullock, EMEA head of portfolio construction and strategy at Janus Henderson.

He adds: “These are the kind of environments where the best opportunities emerge.”

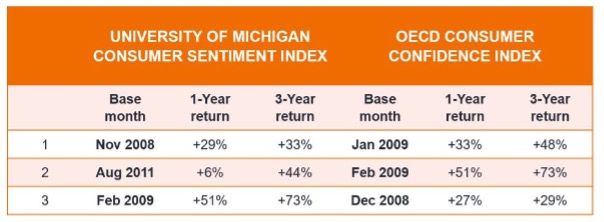

Research suggests that equities often outperform for a few years after periods of low consumer confidence, as measured by indices such as the OECD Consumer Confidence Index.

One and three- year global equity return following worst sentiment indicators

Source: Janus Henderson. Global Equities Returns as measured by the MSCI World Index, Bloomberg. Organisation for Economic Co-operation and Development (OECD).

Assets that are inflation winners

This is certainly an environment that highlights the need for skilled active managers. For example, small-caps often do well when dull sentiment begins to brighten, but 20% of companies in the Russell 1000 index are currently non-earning, which is double the long-term average. Investors therefore need to be looking for low levels of debt, a moat framework and solid revenue.

“Investors should consider tilting towards market areas that will be strongly correlated with inflation pressure over the next decade,” says Samson. “We believe listed renewables and infrastructure are a good investment, correlated with the inflationary pressures of decarbonisation and fiscal spending.”

Of the eight renewable energy infrastructure trusts with five-year track records, the four best performers over that period (to 1 June) with returns of 58.8%, 56.3%, and 49.1% are Greencoat UK Wind (LSE:UKW), JLEN Environmental Assets Group (LSE:JLEN), Bluefield Solar Income Fund (LSE:BSIF), and Renewables Infrastructure Group (LSE:TRIG). The other four investment trusts have returns ranging from 35.9% to 28.8%.

Elsewhere, many pros would recommend REITs and energy stocks as inflation hedges. However, Samson points out “this is at odds with today's stretched housing prices relative to income and mortgage rates, and the need to move towards decarbonising the global economy”.

Meanwhile, healthcare has pricing power and should benefit from demographic changes. Despite the sector’s disappointing 2022, innovation has accelerated with soaring drug approvals by the US Food and Drug Administration, and biotech is particularly cheap with some companies trading below the levels of cash on their balance sheets.

- Holding back the years: three timeless longevity stocks

- Are lifestyle retirement funds right for the 100-year life?

- This massive healthcare business should be worth even more

Worldwide Healthcare (LSE:WWH) Trust offers exposure to major pharmaceutical companies, while International Biotechnology (LSE:IBT) invests in earlier stage and smaller biotech pioneers and pays a more attractive yield of 4.9%.

Why European stocks are looking attractive

Europe is also attractive, owing to its bias to consumer stocks, car manufacture, financials and materials, and pays dividends that are nearly double those of US shares. It particularly stands to benefit from the pick-up in post-pandemic demand and export activity following China’s decision to lift its lockdown.

- Why this unloved fund sector is topping the performance charts

- The active funds investors have been turning to

- The investment boom you could profit from

William Barlow, chief executive officer at Majedie Investments, points out: “Most of my clients have been overweight the US, but right now, we’re looking at European equities, which are much more cyclical, as cyclical stocks are typically first into a recession and first out.

“Just 29% of the S&P’s constituents are cyclical, compared with Europe ex-UK at 42%, and the UK at 52%. European stocks are also cheaper versus history.”

The region also boasts outstanding companies that Goldman Sachs dubs the ‘Granolas’, namely GSK (LSE:GSK), Roche Holding AG (SIX:ROG), ASML Holding NV (EURONEXT:ASML), Nestle SA (SIX:NESN), Novartis (SIX:NOVN), Novo Nordisk (XETRA:NOVA), L'Oreal SA (EURONEXT:OR), LVMH (EURONEXT:MC), AstraZeneca (LSE:AZN), SAP SE (XETRA:SAP) and Sanofi SA (EURONEXT:SAN, which demonstrate strong earnings, robust balance sheets and growing dividends. Many have made good acquisition decisions and invested heavily in R&D.

Do not rule out cash

Given the prevailing macroeconomic backdrop, investors should not denigrate cash, points out Neil Birrell, chief investment office and manager of the Premier Miton Diversified Fund range. As Birrell notes, you can earn around 4% to 5% on money market funds.

Cash also affords investors the chance to take a bite at other opportunities as they arise. Royal London Short Term Money Market fund and Premier Miton UK Money Market fund are two of the better-paying funds.

“If I go round and talk to my fund managers, it doesn’t matter whether they are focused on infrastructure, or US equities, or pan-European REITs, they will all tell me that there are great opportunities out there right now,” says Birrell.

He adds: “REITs, for example, are hugely discounted. But the managers are not sure they want to be buying them today. The market is driven by sentiment, geography, sector, size of company and liquidity, and the influence of each varies at different times. Macro factors have for a while been driving investment, but (I’ll be pleased) when it switches back to bottom-up fundamentals.”

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.