Global Economic Outlook: Recession, Interrupted

27th June 2023 12:59

by abrdn Research Institute from Aberdeen

Wage growth, robust service sectors, and stubborn underlying inflation mean that central banks are not done raising interest rates. But markets are overlooking the scale of the rate cuts that will follow. Read on to find out more…

Resilient labour markets, strong service sectors, and sticky underlying inflation mean that central banks are not done raising interest rates.

However, the size of these hiking cycles is still likely to cause eventual recessions in many developed markets and some emerging economies.

While headline inflation will continue to drop sharply, only these downturns will be able to bring sticky underlying inflation down in a sustainable manner.

In turn, we are forecasting central bank cutting cycles during 2024 that will ultimately take interest rates back into accommodative territory.

Recession, interrupted

The US, and broader global consumer and services sectors, will remain robust for slightly longer than we’d previously anticipated, given households’ ongoing willingness to draw down excess savings, the resilience of labour markets, and the boost consumers will soon get from lower headline inflation.

Certainly, the weakness in manufacturing and housing activity in the US that started in the fourth quarter last year does not seem to have been the usual early-warning signal of a wider recession. Instead, it has remained largely consigned to those two sectors, and there are even signs that housing activity may be starting to recover.

Against this, we expect ongoing stresses in the banking sector amid higher interest rates, although we don’t anticipate a systemic financial crisis. Nonetheless, credit conditions will continue tightening – a headwind to growth that will build over time.

Stubborn inflation

Headline inflation will continue to drop sharply over the next 12 months driven by energy base effects and lower food inflation, albeit with some volatility and cross-country differences. Indeed, by late-2024, headline inflation rates in many economies will be close to target.

Core inflation will also decline from here, as it has already started doing in the US, Eurozone, and many emerging market (EM) economies. However, this will be mostly driven by global-goods disinflation in the first instance. We think core services inflation will remain sticky amid tight labour markets and strong wage growth.

Indeed, a recession is ultimately necessary to bring core-services inflation back to target-consistent rates in the US, many other developed markets (DM), and parts of EMs. We think this is a price central banks are willing to pay to deliver on their mandates and maintain the credibility of inflation targets in the future.

What now for monetary policy?

This means that central banks still have a small amount of additional monetary policy tightening left to implement. We are forecasting a Federal Reserve (Fed) rate hike in July after skipping one in the June meeting. A final rate hike later in the year, as signalled by the Fed’s latest forecasts, is possible although not our base case.

We think the European Central Bank (ECB) will hike rates once more in July, and the Bank of England (BoE) at least twice more. But the risks around these forecasts are also clearly skewed to the upside. Ongoing inflation persistence could force both central banks to tighten further despite the clear desire of policy makers to draw the hiking cycle to a close for fear of triggering recessions.

In Japan, we expect the Bank of Japan (BoJ) to deliver effective monetary policy tightening this northern hemisphere summer via changes to the yield curve control (YCC) framework, allowing the 10-year Japanese Government Bond yield to trade up to 75 basis points.

Past tweaks to YCC reflected concerns about market functioning, which have since diminished. Instead, in a striking change to the Japanese macroeconomic environment, we think the BoJ will now be tightening policy directly in response to a pick-up in underlying inflation pressure.

Recessions around the corner

We continue to think this large monetary-tightening cycle will ultimately lead to recessions in the major DM economies and parts of EMs. The manufacturing sector in many economies is already in contraction. However, amid broader data resilience, we now think the timing of economy-wide recessions will be somewhat later than we had previously anticipated – mostly beginning around the turn of the year.

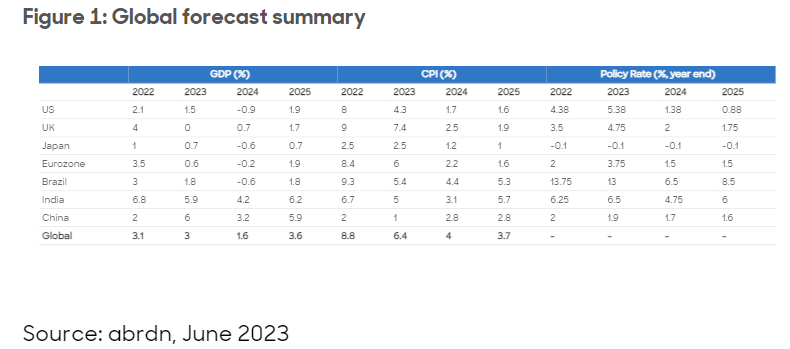

There are cross-country differences in the timing of the respective recessions we are forecasting, with the UK downturn beginning as soon as the second quarter (albeit in part due to a technical quirk of the data), the Eurozone expected to be in recession by the fourth quarter this year, and the first negative quarterly gross domestic product (GDP) print in the US in the first quarter of next year.

That said, our conviction around the precise timing of the US downturn is less strong than our conviction that this cycle will end with a policy-induced recession over a time horizon that is relevant for investment decision making.

The US…

We think policy only became contractionary in the US around the middle of last year when the real policy rate started to exceed our estimate of the equilibrium real rate. The ‘long and variable‘ lags of monetary policy mean that the impact of that tightening is only now starting to be felt in earnest, with the effects set to build through the second half of this year. This is the same signal that our recession probability models are providing, with near-term risks having declined as data have been solid, but longer-horizon models remaining elevated due to the deep imbalances in the US economy.

It is plausible that the economy could remain even stronger than we expect through the rest of this year, with a tight labour market supporting household spending. However, we think such a ‘no landing’ scenario is unsustainable as the Fed would be forced to take another ‘bite of the cherry’ – pushing up rates much further to squeeze out the inflationary excess in the economy. In this scenario, the recession is merely delayed rather than avoided.

…and elsewhere

In our base case scenario, we think monetary policy cutting cycles will begin by early 2024 and continue throughout next year as headline inflation drops and growth is negative. We ultimately expect interest rates to fall below neutral and by more than markets have priced. This is consistent with how theory and history suggest central banks behave, with large and rapid easing cycles the norm once an economy has entered a recession and unemployment is increasing.

The easy gains of China’s re-opening recovery are over. However, we still forecast above-target GDP growth in 2023 given the room for consumption, travel, and services activity to return to pre-pandemic levels. But manufacturing, trade and real estate will continue to struggle, which mean much smaller global economy spill overs than during a typical Chinese recovery. With inflation rates very low, there is scope for modest policy easing.

While many EMs were early to the rate-hiking cycle, they will have to wait until 2024 for underlying inflation to cool enough to allow rate cuts to begin. Latin America is best placed to cut given high real rates. Asia Pacific benefits from a less challenging inflationary environment, but lower policy rates there require a ‘wait and see’ approach. Central and Eastern Europe’s lack of central bank credibility amplifies its still substantial inflation problem, implying the region will be the last to cut rates.

The most likely alternative scenario is still a soft landing. One way of reading the US labour market data is that a benign loosening – that can reset wage growth and lower inflation expectations without a recession – is already underway.

But we still think that historical precedent lends greater weight to a recessionary baseline.

abrdn's Research Institute produces original research at the intersection of economics, policy and markets.

ii is an abrdn business.

abrdn is a global investment company that helps customers plan, save and invest for their future.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.