Five hot takes from Capital Group’s midyear outlook

No one likes to be late to the party – and that’s especially true for investors. Luckily, Capital Group sees the stock market festivities going on a bit longer, writes Theodora Lee Joseph.

28th June 2024 10:32

by Theodora Lee Joseph from Finimize

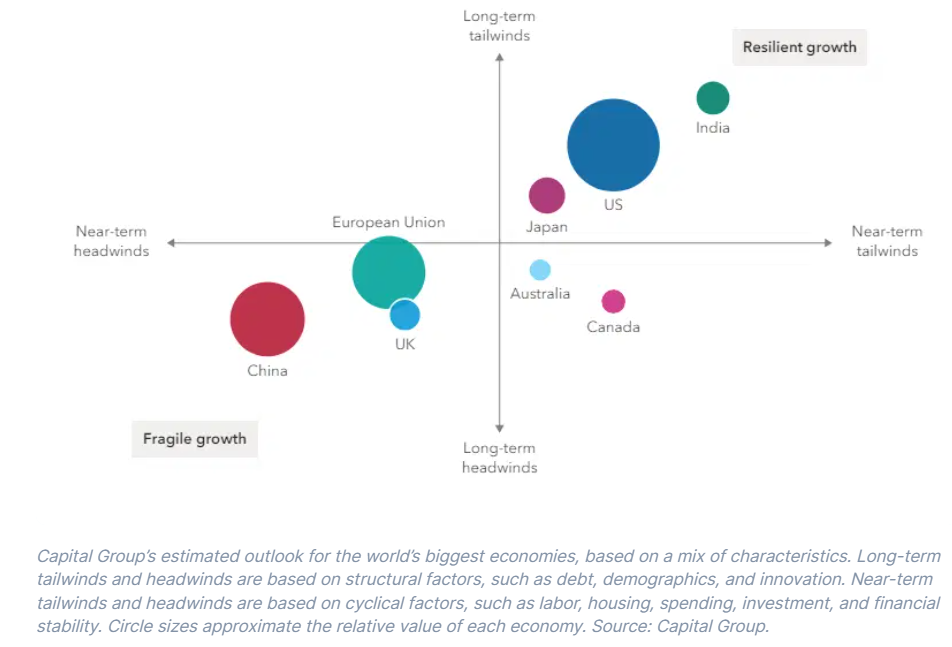

Capital Group believes the US will lead global economic growth while the earnings outlook is equally healthy. The fund is forecasting a 3% economic growth rate this year, thanks to robust consumer spending, a tight labor market, and diversified supply chain investments.

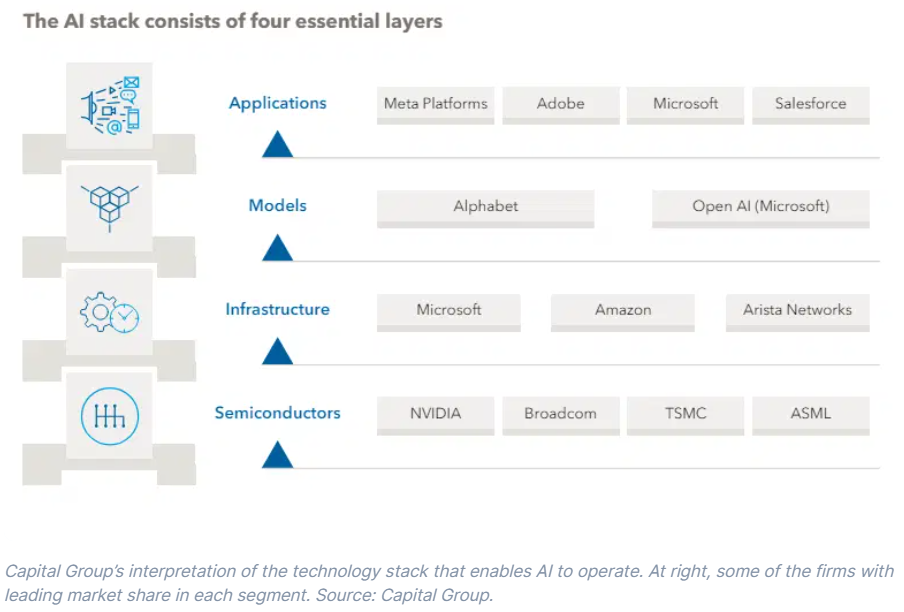

Investing in AI presents significant opportunities, particularly in the tech and utilities sectors. The energy sector is also poised to benefit from the increased demand for electricity by AI data centers.

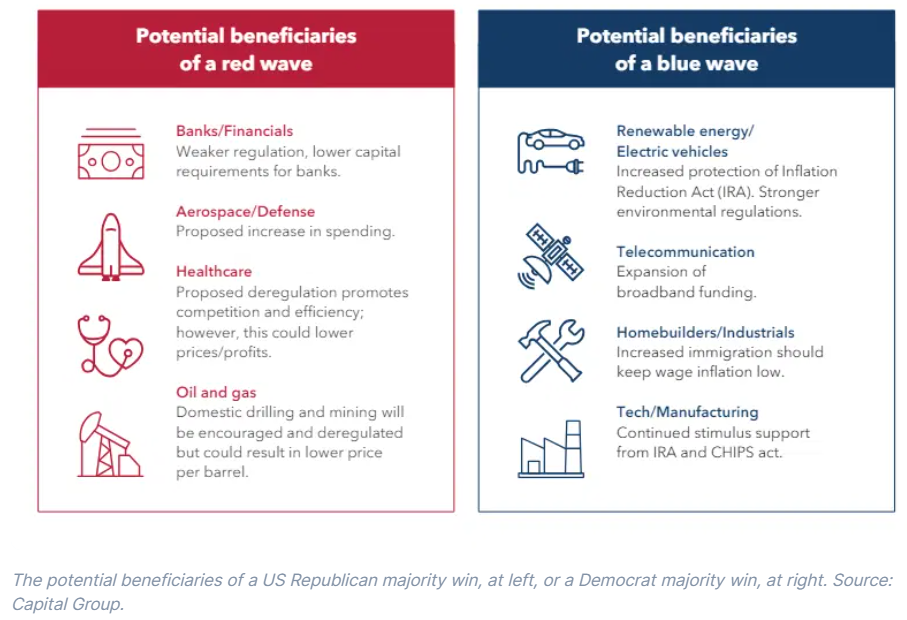

Upcoming US elections could influence various industries differently. A sweeping Republican win could benefit banks, healthcare providers, and oil companies, while a Democratic win could boost renewable energy firms, homebuilders, and the tech sector. But no matter how the election day balloons fall, you can expect some market volatility.

No one likes to be late to the party – and that’s especially true for investors. Luckily, Capital Group sees the stock market festivities going on a bit longer. In its midyear update, the century-old investment house offers a largely upbeat outlook for the global economy, highlights the shiny sectors in the US and Europe, and pinpoints the industries with the most to gain (or lose) in this US election.

Here’s what you need to know to stay ahead.

1. American consumers are giving a much-needed boost to global growth.

The US is the global growth life of the party this year. Capital Group says the world’s biggest economy will expand by 3% this year, helped by strong consumer spending, a tight labor market, and massive supply chain investments. The International Monetary Fund is basically nodding along in agreement: it expects the US economy to grow more than twice as fast as other major developed countries – despite the country’s high interest rates and lingering inflation. Compare that to Europe, which it sees growing at a measly 0.8%.

2. Corporate America’s earnings are expected to boom.

Capital Group’s outlook for corporate earnings is chipper, and – since profit growth drives returns – that’s reason enough for stock investors to keep wearing those party hats. While Wall Street analysts expect S&P 500 company earnings to rise over 10% in the second half of the year (with more gains in 2025), the folks at Capital Group predict a rise of up to 15% this year.

And, sure, the market’s been rallying, but they don’t see stock valuations as overly stretched, with price-to-earnings ratios still close to their ten-year averages. That said, there are potential risks to these rosy estimates, including stubborn inflation, oil price fluctuations, geopolitical tensions, or other unforeseen, wildcard events.

3. Tech and utilities are AI’s brightest prospects.

Investing in AI isn’t a one-size-fits-all deal: it’ll vary as the technology’s matures. Right now, investors should try to get a grip on the AI “stack” – those four layers of tech that make the whole thing tick. Companies are hustling to shine in each layer: semiconductors, infrastructure, applications, and the AI models themselves. The trick is to spot the ones with the brains and bucks to win the race.

Big players like Alphabet Inc Class A (NASDAQ:GOOGL), Meta Platforms Inc Class A (NASDAQ:META), and Microsoft Corp (NASDAQ:MSFT) are splashing tens of billions in hopes of dominating multiple layers of the stack. And while they’re busy with their own processors, top chipmakers like NVIDIA Corp (NASDAQ:NVDA), Broadcom Inc (NASDAQ:AVGO), and Micron Technology Inc (NASDAQ:MU) are likely to keep their market share on lock for years. Finally, let’s not forget the energy sector: AI data centers guzzle electricity like there’s no tomorrow, which is making this sector hot stuff as demand for energy sources, including nuclear, soars.

4. Europe’s aerospace industry is its hidden gem.

Capital Group has its sights set on the, ahem, high-flying aerospace industry, and with good reason. With passenger numbers soaring and supply chains feeling the squeeze, the sector could be on the brink of a super-cycle. That means there could be plenty of runway ahead for above-average demand growth. But the real kicker could on the supply side, with back orders for new aircraft stretching all the way to 2030. Markets like India and China are filling up the order books as their huge middle classes take to the skies. In an industry dominated by the US’s Boeing and France’s Airbus, the resulting pricing power is hard to ignore.

What’s more, industry leader Airbus recently pared back its plane delivery targets owing to supply-side challenges, showing that it’ll be tougher to meet this new demand. What this also means is that older planes are likely to fly for longer, which means more maintenance. Almost 70% of commercial aircraft in use are over five years old, and 32% are over 12. This boosts companies in the aftermarket service game, which is already a high-margin business. Suppliers like France-based Safran SA (EURONEXT:SAF) and UK-based Melrose Industries (LSE:MRO) are raking in recurring revenue from work done on existing products. In fact, the money made from replacement parts often surpasses the initial sale, as aircraft components are serviced multiple times over a plane’s lifespan. These durable revenue streams offer a rock-solid foundation for long-term investment potential.

5. US elections could benefit certain sectors disproportionately.

US stocks typically perform better post-election no matter who wins, but the impact on various sectors can vary. This year, much will depend on whether the winning presidential candidate can rally enough support to secure victories for “downballot” candidates, potentially giving their party control of both the US Senate and the House of Representatives in one fell swoop.

In a “red wave” scenario with Republican dominance, shares of banks, healthcare providers, and oil and gas companies could benefit, as folks anticipate deregulation moves. Conversely, a “blue wave” of Democratic control could boost shares of renewable energy companies, industrial names that could be involved in infrastructure projects, and telecom firms that might snag funding for a nationwide broadband expansion.

A gridlock scenario, in which neither party gains full control, likely wouldn’t change much for the market. But, no matter what happens, you can expect some occasional market volatility in the lead-up to the November 5th election.

What does this mean for you?

To put it simply: there’s still plenty of action in specific markets. When stock indexes hit record highs, some folks think they’ve missed the gravy train. But that’s just plain wrong. Markets have a well-earned reputation for trending higher and peaking multiple times. If the past is anything to go by, bull markets are marathons, not sprints – lasting two to five years and rewarding investors with an average gain of about 178%.

Sure, market dips happen, and stocks can drop at any time. But history shows that new highs are often prime entry points for long-term investors. Since 1950, the S&P 500 has delivered a sweet 17.1% average return in the 12 months after the index has hit an all-time high. Gains over those periods were almost a sure bet – except during the global financial crisis.

Bull markets can last a long time, but they don’t last forever: they’re just one part of the market’s ebb and flow. Recognizing where you are in the cycle and what might happen next can keep you grounded and help you maintain some all-important long-term perspective.

Theodora Lee Joseph is an analyst at finimize.

ii and finimize are both part of abrdn.

finimize is a newsletter, app and community providing investing insights for individual investors.

abrdn is a global investment company that helps customers plan, save and invest for their future.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.