A decade of pension freedoms: what you’ve done with your money

As George Osborne’s retirement revolution turns 10 years old, Craig Rickman explores how the pension income landscape has turned on its head, reveals the retirement income strategy of choice and looks ahead to what the future might have in store.

2nd April 2025 13:41

by Craig Rickman from interactive investor

Let’s see a show of hands: who’s raided their pension savings in the past 10 years and splashed out on a Lamborghini?

As some of you will recall, that was the stark - and presumably tongue in cheek – warning issued by ex-pensions minister Steve Webb, after then-Chancellor George Osborne shockingly tore up the retirement rule book at his 2014 Budget.

The radical reforms, called the pension freedoms, took effect the following year, and put you in the driver’s seat, allowing you to draw from your retirement savings however you wish from age 55. “No caps. No drawdown limits. Let me be clear, no one will have to buy an annuity,” Osborne famously crowed.

So, after a decade behind the wheel, how have savers embraced their newfound liberation, and what shifts have we seen?

- Invest with ii: SIPP Account | Stocks & Shares ISA | See all Investment Accounts

To answer these questions, we of course need some data.

Fortunately, the Financial Conduct Authority (FCA) has been collecting tonnes since April 2015, specifically on how pension pots are accessed for the first time. As the numbers for 2024-25 are not available, we unfortunately don’t have the full 10 years’ worth. There are also some gaps early on and not all firms took part in every data period. But nevertheless, there’s more than enough to grasp what people have been doing.

Here I delve into two different data sets. The first looks at how savers have interacted with individual pots, while the second examines the size of assets piled into each pension-access option.

New rules, new behaviours

Simply put, the people have spoken. And they want flexibility.

Before the freedoms most people bought an annuity, where you trade your pot for the certainty of a guaranteed income for life, or a set period. According to the Pension Policy Institute, 90% of defined contribution (DC) pension assets ploughed into them before 2015, peaking in 2009 at 466,000.

But since the reforms, and as widely expected, annuities have fallen heavily out of favour. Just over six million pension pots were accessed for the first time between April 2015 and March 2024, and only around one in 10 bought a guaranteed income.

Annuity sales plummeted to fewer than 80,000 in 2015-16, tumbling below 60,000 seven years later. Things have picked up a bit recently after guaranteed income became more attractive in response to higher interest rates, with sales hitting 82,061 in 2023-24 – the best year since the freedoms were introduced. We should note, however, this was during a 12-month period when the volume of pension pots first accessed also peaked.

The remaining nine out of 10 pots were drawn flexibly, either taken in one hit, moved to income drawdown or partially accessed, emphatically illustrating that savers have embraced the new landscape.

Let’s examine drawdown first as it provides the alternative to annuities for people seeking a regular income in retirement.

- Watch our video on pensions and IHT: what you need to know about 2027 changes

- My pension goals for 2025

Since 2015, the numbers show that just under 1.7 million pots (27%) taken for the first time have gone into income drawdown, where you remain invested, and take money out whenever you please - an attractive option for those who crave flexibility and are happy to leave risk on the table.

However, an absence of drawdown data during the first three months of freedoms means this figure is likely closer to 30%. Either way, drawdown sales have outstripped annuities three-fold, becoming the retirement income strategy of choice.

Another flexible withdrawal method, and one not to be confused with drawdown, is uncrystallised funds pension commencement lump sum (UFPLS) – a rather ambiguous piece of jargon.

The way UFPLS works is that 25% of what you take is tax free, while the remainder is taxable, a useful strategy for anyone who wants to make a partial withdrawal without committing to drawdown or an annuity. You can also preserve any remaining valuable tax-free cash (most people can take 25% capped at £268,275), which could give rise to a bigger amount in the future if your fund grows.

UFPLS made up roughly 6% of pots accessed for the first time, gradually increasing in popularity as the years passed, illustrated by the table further down.

This brings us to the final pension-access option – full encashment. Interestingly, more than half of plans were withdrawn using this method, which prompts the question: were Webb’s fears realised, and savers indeed spent lavishly on supercars?

The data suggests this is almost certainly not the case as around two-thirds of pots taken in full were less than £10,000, while around nine in 10 were £30,000 or smaller.

We must not overlook that these figures refer only to individual pots. It’s possible and indeed inevitable that some people will have fully encashed a few, but we can still rule out extravagant purchases for the most part. A further reason is that pension income, other than your 25% tax-free entitlement, is taxable, meaning big withdrawals can lead to big HMRC bills.

Another consideration is that people may have done different things with different pots. For instance, taking out a smaller pot in full, and moving a larger one into drawdown.

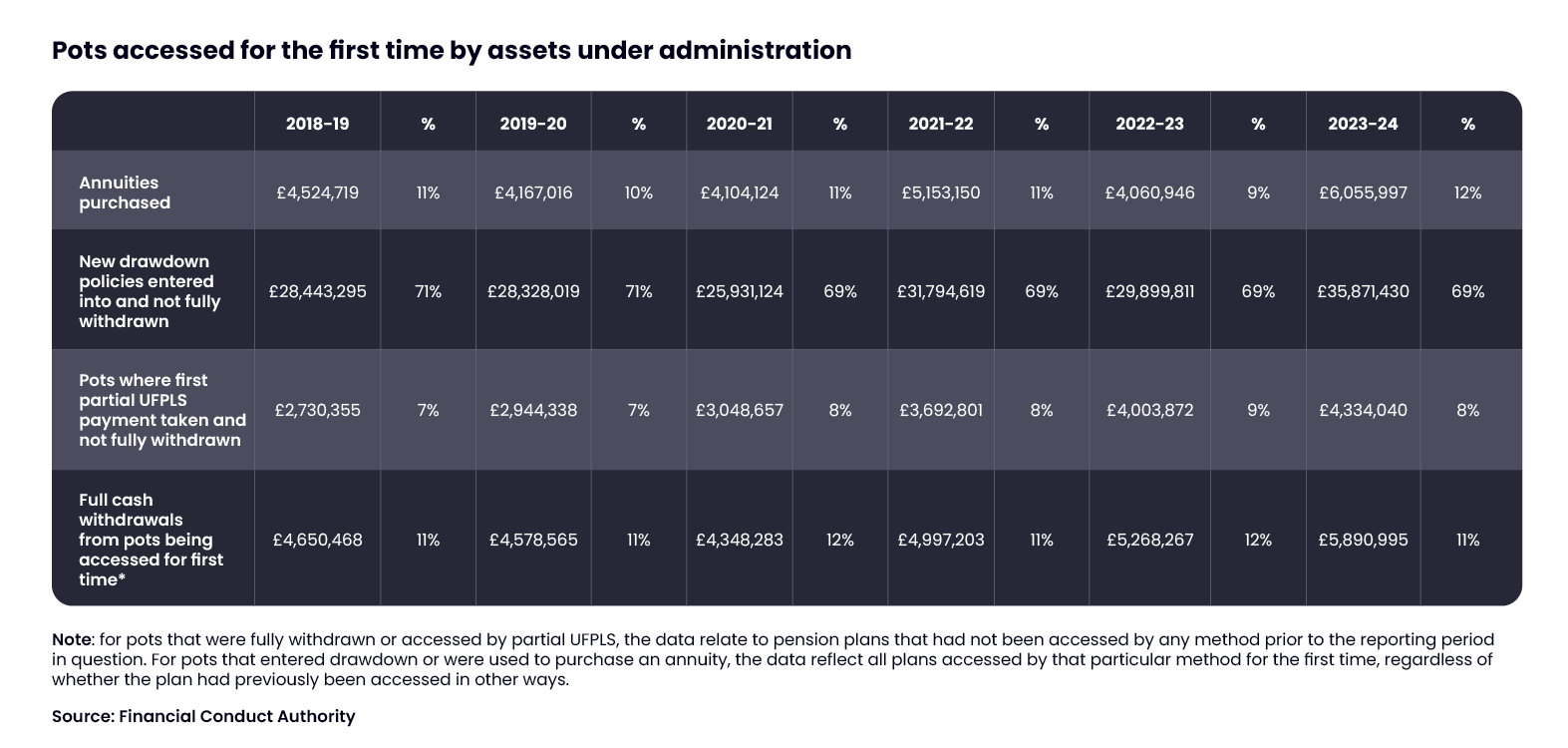

Big money goes into drawdown

Looking at how savers have drawn individual pots is only one side of the coin. The other is the monetary consideration for each withdrawal method, which paints a rather different picture as the table below shows.

While we don’t have the full data set here as the FCA didn’t collect it before 2018, during the past six years around £7 in every £10 of pension money accessed for the first time entered income drawdown, showing it’s by far the preferred strategy for those with significant savings.

As stated above, while more than half of pots were fully cashed in, these amounts were typically small. Only £1 in every £9 has been withdrawn using this method.

The numbers also capture the recent uptick in annuity popularity, although this is coming from a small base. Despite the mini revival, drawdown has still dwarfed annuity money.

Another notable upward trend can be seen with UFPLS. The strategy has gained significant popularity since 2018, presumably due to greater consumer awareness of the options available, leading to more informed decisions.

Are people doing the right thing?

Whether enough people are knocking on financial advisers’ doors is unknown. Only around a third of pension pots are accessed after receiving regulated advice, which isn’t a frighteningly low number given only 10% of the population take advice every year. However, we should note that how you choose to draw from your pension pots is among the most complex and important financial decision you’ll ever make.

The attractions with drawdown are obvious: you get to stay in control, benefit from potential future investment growth, and perhaps leave a legacy – although the proposal to end pensions’ inheritance tax (IHT) exemption might stick a spanner in the works of this perk.

- Q&A podcast episode: tackling your pension and investment questions

- Ask ii: should I use a SIPP or ISA to boost my retirement savings?

But to make sure your savings pot lasts a lifetime it needs a personalised strategy and a regular service. Big decisions about how to invest and how much to draw every year don’t cease at the point you enter drawdown.

A couple of pieces of research since freedoms unearth the possible risks and sentiment here.

Back in 2018, the FCA found that one in three who’d gone into drawdown didn’t know where their money was invested. And ii’s Great British Retirement Survey 2021 found that 27% of people in retirement worried about running out of cash in old age. This figure had fallen marginally to 24% two years later.

Looking ahead – what might the next 10 years have in store?

Savers will inevitably face a different set of opportunities and challenges in the coming decade.

For those undecided about drawdown, an annuity, or a bit of both, help could be on the way, in the shape of the FCA’s targeted support, a way for pension providers to guide people towards suitable financial products. This could be a game changer, supporting those who need a bit of help but don’t want, need or can’t afford financial advice.

We should hopefully learn more about how the initiative might look later this year.

Meanwhile, some key pension rules are changing too.

The minimum age you can draw pensions will rise to 57 from 2028. Something to be aware of if you fancy retiring early.

In other developments, while Labour abandoned plans to reinstate the pensions lifetime allowance (LTA) - which placed a ceiling on what your savings could be worth before facing hefty tax charges - they delivered a thunderous blow at their first Budget in 14 years just a few months later; proposing to bring unspent pensions into the scope of IHT from 2027.

While the policy remains in the consultation stage and has faced fierce opposition due to potential eye-watering rates of double taxation and hideous complexity, a stark U-turn seems remote.

- Is it possible to give away my pension savings to avoid IHT?

- Why did pension pots for over 55s plummet during Covid?

The early thinking is that savers will drain pension assets earlier than originally intended and more people will buy annuities, as the allure for passing pension assets to younger generations on death is likely to reduce.

The latter is very much a possibility, but as the table above shows, there’s a lot of ground to make up. A recent ii survey found 58% of people have no plans to buy an annuity, citing poor value for money, and a desire for greater control.

A factor challenge concerns investment performance. Other than a couple of sticky patches, a notable one at the start of Covid, markets have fared rather well since freedoms, rewarding those who’ve kept their pension money invested.

But there’s no guarantee the coming years will prove equally fruitful. Investment volatility is one of the biggest risks for retirees who choose flexibility over guarantees, especially in the early years when a market slump could affect how long your money lasts. If global stocks do take a turn for the worse, the decisions you make will carry even greater weight.

Ultimately, from pension rules and tax changes to market performance, we don’t know for sure how the next 10 years of freedom and choice will pan out. One thing is certain, the decisions you make at and during retirement won’t become any less important.

When considering your pension income options, remember the road in later life might be long, so whether you splurge on a Lambo or not, make sure your retirement savings don’t run out of gas.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.