13 trusts to play Europe’s stock market revival

The Continent is ‘having a moment’, argues one Kepler analyst, who examines various ways to invest in Europe.

28th March 2025 14:00

by Alan Ray from Kepler Trust Intelligence

This content is provided by Kepler Trust Intelligence, an investment trust focused website for private and professional investors. Kepler Trust Intelligence is a third-party supplier and not part of interactive investor. It is provided for information only and does not constitute a personal recommendation.

Material produced by Kepler Trust Intelligence should be considered a marketing communication, and is not independent research.

It’s a central tenet of European equity investors that the investment opportunity isn’t dictated by politics or economic performance of the region and, if one was being unkind, one might go further and say that the investment opportunity exists in spite of those.

- Invest with ii: Invest in Investment Trusts | Top UK Shares| Interactive investor Offers

Instead, Europe is home to many leading global companies across a range of sectors, and that’s what investors should really be focused on. That’s the theory, but in practice investor sentiment to Europe has been at a low ebb for some time, with economics and politics seemingly the limiting factors. And so, with the end of the first quarter of 2025 upon us, many seem surprised that European equities have performed strongly, rising by over 8% at an index level. Notably, this performance is significantly better than US equities, which have declined by over 3%, and in many cases by considerably more than that. This, in the view of many European equity fund managers, has been a long time coming, for fundamental reasons to do with undervaluation and good corporate performance but, dare we say it, politics, which we are supposed to ignore, has provided the catalyst.

It feels unnecessary to go into detail about the belligerent approach the US is taking with its bewildered allies, but one consequence is that investors, already jittery about high valuations on US equities, have been prompted to take a fresh look at Europe, which appears to be behaving in an unusually cohesive and mature manner. In our view, it’s OK to view these events as a catalyst for investors to reappraise European equities, but equally we need to keep a sense of perspective. There’s a narrative developing among the commentariat that ‘Europe has awoken’ and that the US’ post-war role as the stabilising power in the world is coming to an end.

Those might be fascinating topics to debate in years to come, but we need to remember that politics and economics in Europe have a very large capacity to disappoint investors. We can say with quite high confidence, for example, that the path for Europe to collectively spend more on defence and develop a dynamic industrial base to feed that is likely to be full of twists and turns, and retail investors piling into defence stocks might find it’s a wild ride. We can also say that the subject of trade tariffs, cause of so much market volatility, doesn’t appear even close to being resolved.

What we do know is that our group of European equity fund managers consistently identify that Europe has many leading global players in a range of sectors and that European equities are often at significantly lower valuations than their US counterparts. One of the key questions to ask when confronted with the information that one market is ‘cheaper’ than another is whether that is because the ‘cheap’ market has a different mix of sectors that usually trade at lower valuations. European equity fund managers have been asked that question so often that we find that they consistently forestall the question by observing this is true across individual sectors and often at an individual stock level. Thus, healthcare giant Novo Nordisk AS ADR (NYSE:NVO) is often described by our fund managers as trading at a lower valuation than its closest competitor Eli Lilly and Co (NYSE:LLY), the other dominant player in the GLP-1, or weight-loss drug, market. We’re obviously not qualified to say exactly why that may be, but we do know it’s a consistent theme among fund managers.

Furthemore, while Europe has ‘always’ traded at a lower valuation than the US, over the last 10 or more years the composition of the market has changed, with sectors such as healthcare and technology superseding solid but unexciting sectors like energy and banks. A great many of Europe’s technology growth businesses fall under the category ‘industrial’ because, well, they are, and this may be one reason why perceptions about Europe are different to reality. Indeed, many of Europe’s best technology names are not, in contrast to their US counterparts, household names because their businesses are aimed at other businesses, rather than directly at consumers.

So, the make-up of the European market has shifted to more growth-orientated sectors unnoticed by some and so the argument that Europe should always be at a discount to the tech-heavy US market is less persuasive than it was a decade or two ago. The two markets are not the same, and we think the US’ premium is likely to be deserved for the foreseeable future, but the gap may be wider than is deserved.

Is it too late?

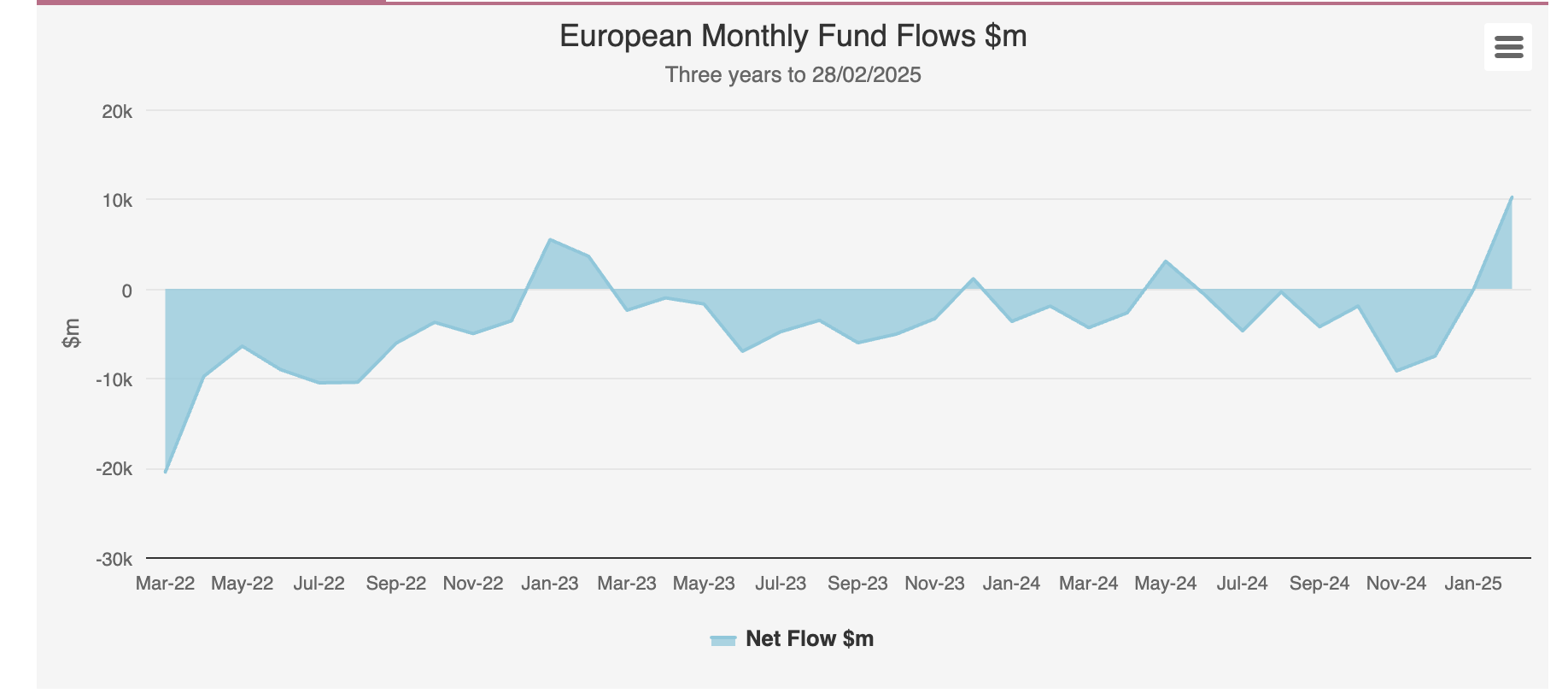

When things go up, it’s always a good question to ask. Let’s look at those most interesting of indicators, the monthly fund flows in and out of European equity funds. The chart below plots the net flows monthly over the last three years and, as it shows, February saw a big jump into positive flows. The amount, $10 billion, seems to indicate a big jump in investor sentiment.

Monthly fund flows

Source: Morningstar

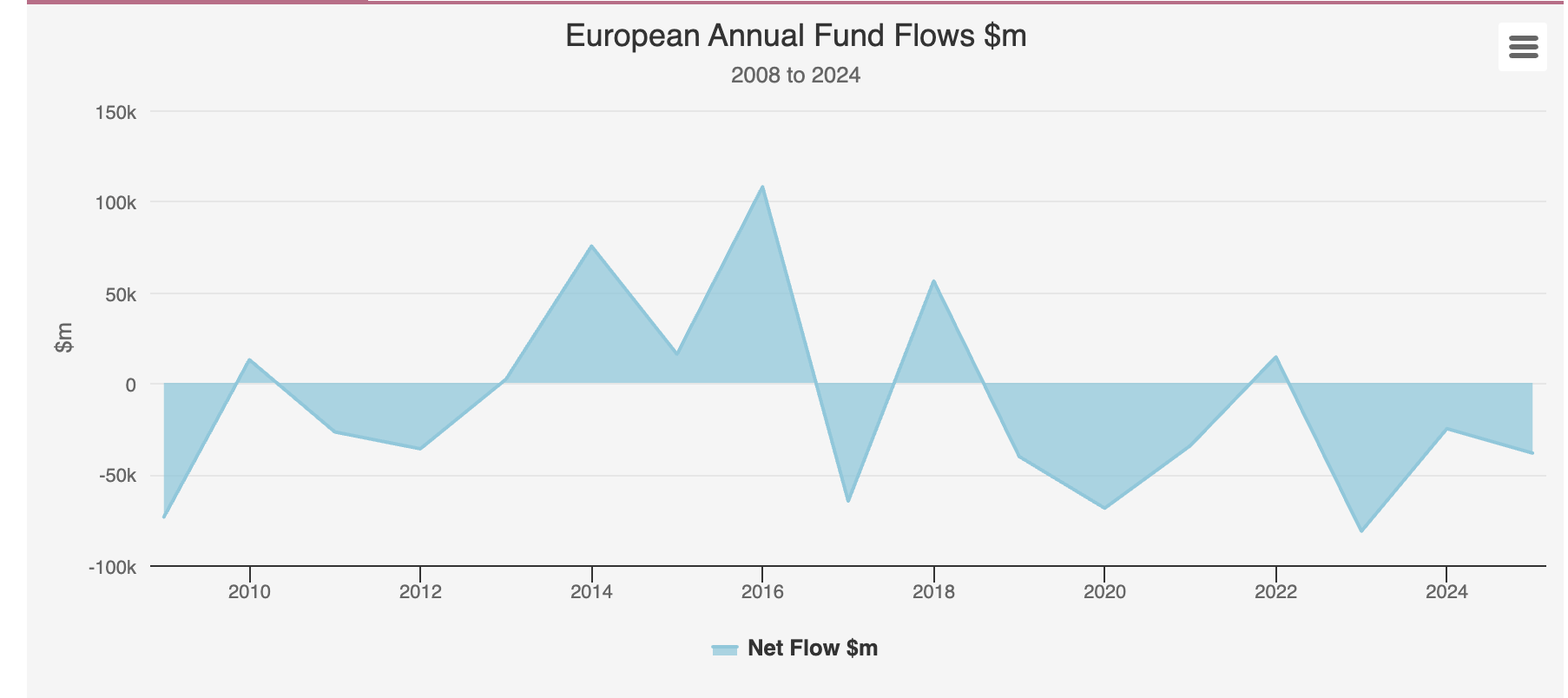

The next chart is a data series going back to 2008 to give us a greater sense of the long-term attitude to European equities. This also helps put that jump in February into context. From 2020 through to 2024 investors pulled $164 billion from European equity funds on Morningstar’s database. As we say above, investor sentiment has been at a low ebb for some time, and a $10 billion inflow in February is just a small start in addressing that. So, while of course other headwinds could come in to play, the unwinding of excessive optimism from investors doesn’t seem to be one of them.

Annual fund flows

Source: Morningstar

What investment trusts are there to choose from?

Moving on to the practical matter of how one goes about investing in Europe, the investment trust sector has a good selection of European specialist investment trusts that have delivered good performance in the past. As ever, it seems that investment trust investors know something the rest of the investing community doesn’t.

Below we look at each of these, with some broad descriptions of how each might fit within a portfolio. Because we know dividends are an important topic for many investors, there is a separate section further below that runs through the main dividend-paying trusts. For a deeper look at any of them, you can visit the individual trust pages for the latest research.

Large-caps

While it is hard to pin down exactly what a ‘core’ investment strategy really is, let’s start with the trust that is most explicitly targeting that category. JPMorgan European Growth & Income Ord (LSE:JEGI)seeks to incrementally outperform its benchmark with a broadly diversified portfolio. The team managing JEGI seek to generate most of their outperformance through stock selection, overlaid with JPMorgan’s value, quality and momentum approach, and generally avoid taking big sector and geographic bets against their benchmark. This approach has generated very consistent returns, and JEGI’s strategy has proved very adaptable to different types of markets. As we discuss later, JEGI also pays a healthy dividend from a mixture of revenue and capital and yields over 4%.

Fidelity European Trust Ord (LSE:FEV), which is the largest of the European trusts with a market cap above £1bn, also makes a very good case to be considered a core European equity exposure. While the team managing it target capital growth, and have an excellent track record in this, one of their key considerations when assessing a company is its ability to pay a dividend. With no specific income target, this doesn’t translate to an especially high yield, although in a later question about income we note FEV’s strong dividend growth, but the more conservative characteristics of dividend-paying companies may be something that appeals to investors seeking a core exposure, even if they don’t particularly want income.

BlackRock Greater Europe Ord (LSE:BRGE)could also be considered as a core holding, albeit with a more overtly growth-orientated approach and a focussed portfolio of 20 to 30 stocks. Manager Stefan Gries recently spoke at one of our online events about his sense of optimism about investing in Europe. Use the tools here to register to be notified when the recording goes live.

European Opportunities Trust (LSE:EOT)provides investors with a different approach to Europe from the rest of the peer group, with a pan-European portfolio that includes the UK. The managers of EOT very much focus on companies that are global in nature and often have significant revenue outside Europe, notably in the US. EOT’s performance in the past five years has been marred by some individual stock decisions that have gone wrong, but over the long term this trust has an excellent track record of finding long-term winners, being a notably early investor in index heavyweight Novo Nordisk, and the team managing the trust have made significant personal commitments to owning shares in the trust.

Baillie Gifford European Growth Ord (LSE:BGEU)takes a more definitively growth-orientated approach than others, with a greater proportion of the portfolio in mid-cap stocks and a small number of unlisted stocks. This is a strategy that has had a tougher time in the higher inflation / higher interest rate era and it has seen a couple of write-downs in the unlisted portfolio, but for investors seeking a very strong commitment to growth opportunities further down the market-cap spectrum, this could be a good choice.

Henderson European Trust Ord (LSE:HET)is another good option, with an excellent track record of investing in a very pragmatic way, certainly with an underlying preference for quality growth, but able to embrace value or recovery opportunities. At the time of writing this trust is undertaking a shareholder consultation following the resignation of its two co-managers and we would expect a further update in the coming weeks.

Small-caps

As we saw, it’s too early to conclude that investor sentiment has become excessively optimistic, but equally it’s quite common to expect small- and mid-caps to lag in the first phase of investors rediscovering a market. As this phase matures, one might expect more interest further down the market-cap spectrum and the sector has some good options to capture this next wave.

The European Smaller Companies Trust PLC (LSE:ESCT)could be seen as the most all-encompassing smaller companies trust, as its managers embrace a strategy that takes in mature growth, value situations, turnaround and recovery situations and earlier stage growth companies. ESCT has an excellent track record and notably has outpaced large-caps over the past five years, even during a period when small-caps as an asset class have been out of favour. It is worth noting that ESCT is, at the time of writing, in a good faith negotiation with activist investor Saba, who readers are very likely aware of following extensive coverage and we think it’s likely an announcement relating to this will be made in the coming weeks.

JPMorgan European Discovery Ord (LSE:JEDT) offers a small-cap strategy that shares some of the DNA of its stablemate JEGI, in that factors such as value, momentum and quality are part of the process. JEDT ’s management team was changed in March 2024 and the trust’s performance, which had lagged its benchmark, has shown good progress to restoring its longer-term track record. The trust has taken a very active approach to its discount, using buybacks and a tender offer to help with this.

European Assets Ord (LSE:EAT)takes a broader mid- and small-cap approach and seeks to identify companies that have defensible business models, sometimes referred to as ‘wide moats’, and the team managing it generally favour companies that meet their preferred quality growth criteria. Like JEDT, EAT has seen a change of management personnel, and although this was less than a year ago, performance has stabilised following a tough period, particularly in 2022, when the trust experienced underperformance. As we’ll see in the next section, EAT has a very attractive dividend policy.

Dividends

European equity dividend yields sit somewhere in between the UK FTSE 100’s circa 3.5% and the S&P 500’s 1.5%, at around 2.7%. This indicates that dividends are taken seriously in Europe, but the mix of stocks in the index and the very embedded culture of equity dividends in the UK both help explain the higher yield in the UK, and the prevalence of UK equity income investment trusts. Nevertheless, there are several options available for income-conscious investors among the European trusts.

A quirk of history means that EAT was the first investment trust in any sector to pay dividends partially funded from capital. EAT began its life as a Dutch company with its primary listing in the UK and for all practical purposes functioned exactly like any other investment trust. At some point a switched-on advisor realised that Dutch tax laws allowed for distributions of capital as dividends and so the capital dividend, calculated as a percentage of NAV, was born. It was several years before the UK regulations caught up, by which time EAT had established a loyal following of income investors who saw it as a diversifier from other equity-income focussed trusts. EAT converted to a UK company many years ago and today pays quarterly dividends calculated as 6% of the closing NAV each financial year. Factoring in its discount, it currently yields circa 6.5% although, of course, like any capital dividend, the amount will vary up and down with the NAV, rather than as a traditional progressive dividend.

EAT is a mid- and small-cap focused trust and while those segments of the market can be the source of strong returns, they can also be a source of volatility and more risky. JEGI has built up a very strong track record as a ‘core’ European equity trust, with an excellent record of incremental outperformance of the benchmark, while at the same time its dividend policy is to pay a dividend, similar to EAT, calculated as a percentage of NAV.

FEV is not, explicitly, an equity income trust but its managers tend to favour companies that are able to pay a dividend as part of their search for compounding growth opportunities. FEV’s yield, circa 2%, is similar to the benchmark but its record of dividend growth is very strong and those income investors who are targeting long-term growth in dividends rather than an immediately high yield could consider FEV as a source of potential growth. Further, some investors favour equity income trusts not only because of the dividend per se but, like the managers of FEV, they like what it says about the companies that are invested in, and so FEV may also appeal if this is a consideration.

Similarly, HET, yield circa 2.4%, does not have an explicit yield target but does have a long record of a progressive dividends. BRGE has a yield of just over 1%, which is clearly very low for an income seeker but notably it sits on the AIC’s next generation Dividend Heroes list, having increased its dividend for 18 years, compounding at 7%. In the next section we look at a few investment trusts that offer different exposure to Europe, including some strategies that could appeal to an income investor.

Beyond general equities

While there are of course many trusts with some exposure to Europe, there are a few notable trusts outside the Europe and European Smaller Companies sectors that provide investors with explicit European or pan-European exposure that could provide a good extra layer of diversification.

TR Property Ord (LSE:TRY) is a sector specialist that invests predominantly in pan-European listed property companies, or REITs, together with a small allocation to physical property in the UK. Property is an interest rate and bond yield-sensitive asset class and following a tough time in 2022 and 2023 the green shoots of recovery have begun to show through in 2024 and 2025. A feature of some European property markets is that rents are contractually linked to inflation, and many of TRY’s European holdings have benefitted from this in recent years. TRY’s dividend yield, just over 5%, reflects the underlying asset class’s income characteristics, and TRY also has a very good long-term record of increasing its dividend ahead of inflation.

3i Infrastructure Ord (LSE:3IN) is, as the name suggests, an investor in infrastructure but it distinguishes itself from many of its peers because it is essentially a private equity investor into businesses that themselves own, operate, install or maintain infrastructure assets, so it combines some of the higher returns possible from owning operating businesses with some of the long-term contractual cash flows that are the bedrock of most infrastructure portfolios. In this way, we think it’s a legitimate addition to a portfolio of European equity trusts to provide a different source of returns. Its yield, circa 4%, is low in an infrastructure context but certainly high enough for an equity-income investor and 3IN has a very good record of dividend growth. 3IN is not wholly invested in pan-Europe, with a single investment in Singapore, but can for practical purposes be considered for pan-European exposure.

Europe is no stranger to private equity and while many private equity trusts do allocate some capital to Europe, we would highlight specialist HgCapital Trust Ord (LSE:HGT), which has an outstanding track record as a direct investor into pan-European growth businesses, with an emphasis on areas of technology such as software services. This is a strength for Europe and HGT has built an enviable record over multiple decades of supporting businesses through their growth. CT Private Equity Trust Ord (LSE:CTPE) is a more broadly diversified fund of funds and co-investments in pan-European mid and small buyout funds, positioned just below the highly competitive large buyout market, and has similarly built up a good long-term track record of investing. CTPE also distributes a dividend from capital, equivalent to 4% of NAV, paid quarterly.

Conclusion

One of the reasons that film Love Actually is so enduringly popular is down to the scene where Hugh Grant’s prime minister tells his US counterpart exactly what he thinks, and one would have to have a heart of stone not to enjoy that fantasy being played out on screen by a beloved actor and to daydream about the real-life version.

As investors though we can’t allow ourselves to be carried away with fantasies. Europe, and the UK, is ‘having a moment’, which has helped investors to take another look at its equity markets, but ultimately, it’s up to the companies listed there to show investors what they can do and why they deserve a higher valuation. Luckily for us, there are a number of active investment trust managers who have shown themselves to be incredibly adept at navigating European markets, regardless of whether sentiment, politics and economics are positive or not. In that sense, it’s business as usual.

Kepler Partners is a third-party supplier and not part of interactive investor. Neither Kepler Partners or interactive investor will be responsible for any losses that may be incurred as a result of a trading idea.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Important Information

Kepler Partners is not authorised to make recommendations to Retail Clients. This report is based on factual information only, and is solely for information purposes only and any views contained in it must not be construed as investment or tax advice or a recommendation to buy, sell or take any action in relation to any investment.

This report has been issued by Kepler Partners LLP solely for information purposes only and the views contained in it must not be construed as investment or tax advice or a recommendation to buy, sell or take any action in relation to any investment. If you are unclear about any of the information on this website or its suitability for you, please contact your financial or tax adviser, or an independent financial or tax adviser before making any investment or financial decisions.

The information provided on this website is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation or which would subject Kepler Partners LLP to any registration requirement within such jurisdiction or country. Persons who access this information are required to inform themselves and to comply with any such restrictions. In particular, this website is exclusively for non-US Persons. The information in this website is not for distribution to and does not constitute an offer to sell or the solicitation of any offer to buy any securities in the United States of America to or for the benefit of US Persons.

This is a marketing document, should be considered non-independent research and is subject to the rules in COBS 12.3 relating to such research. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research.

No representation or warranty, express or implied, is given by any person as to the accuracy or completeness of the information and no responsibility or liability is accepted for the accuracy or sufficiency of any of the information, for any errors, omissions or misstatements, negligent or otherwise. Any views and opinions, whilst given in good faith, are subject to change without notice.

This is not an official confirmation of terms and is not to be taken as advice to take any action in relation to any investment mentioned herein. Any prices or quotations contained herein are indicative only.

Kepler Partners LLP (including its partners, employees and representatives) or a connected person may have positions in or options on the securities detailed in this report, and may buy, sell or offer to purchase or sell such securities from time to time, but will at all times be subject to restrictions imposed by the firm's internal rules. A copy of the firm's conflict of interest policy is available on request.

Past performance is not necessarily a guide to the future. The value of investments can fall as well as rise and you may get back less than you invested when you decide to sell your investments. It is strongly recommended that Independent financial advice should be taken before entering into any financial transaction.

PLEASE SEE ALSO OUR TERMS AND CONDITIONS

Kepler Partners LLP is a limited liability partnership registered in England and Wales at 9/10 Savile Row, London W1S 3PF with registered number OC334771.

Kepler Partners LLP is authorised and regulated by the Financial Conduct Authority.