10 years of pension freedoms: SIPP drawdown trends and choices

interactive investor examines trends among its customer base.

3rd April 2025 11:17

by Myron Jobson from interactive investor

With the new tax year marking the 10th anniversary of pension freedoms, interactive investor, the UK’s second-largest DIY investment platform, examines drawdown trends among its SIPP customer base.

The ability to withdraw up to 25% of a pension tax-free (subject to a maximum of £268,275) once you reach 55 (rising to 57 from 2028) is one of the many attractive tax advantages of pension saving. For many retirees, their pension pot must last a lifetime, and perhaps support a loved one as well, so paying as little tax as possible is vital.

- Learn more: SIPPs Explained | SIPP Calculator | SIPP Drawdown

Among interactive investor (ii) customers who moved all or part of their SIPP into drawdown between April 2019 (when comparative records began) and the end of March 2025, 49% chose to take the maximum tax-free lump sum of 25% of their entire SIPP.

Meanwhile, 29% withdrew less than 10% of their pension pot tax-free, and 22% took out between 10% and 24%.

These figures are slightly higher for customers who were age 55, which represents 11% of the broader cohort: 59% withdrew the full 25%, 21% took between 10% and 24%, while 20% took less than 10%.

Cohort | Full 25% | 10-24% | Less than 10% |

All SIPP customers in drawdown | 49% | 22% | 29% |

SIPP customers in drawdown who were age 55 | 59% | 21% | 20% |

Source: interactive investor.

Average age of accessing the 25% tax-free lump sum and regular pension income

Not only are ii customers taking tax-free lump sums and regular pension income earlier than before, but the trend is accelerating.

Before the pandemic, between 2018 and 2019, the average age at which ii SIPP customers took their first tax-free lump sum was 62. By comparison, this had fallen to 61 between the start of 2023 and the end of 2024.

Similarly, the average age for taking a regular pension income has declined - from 66 in 2018-2019 to 63 between 2023 and the end of 2024.

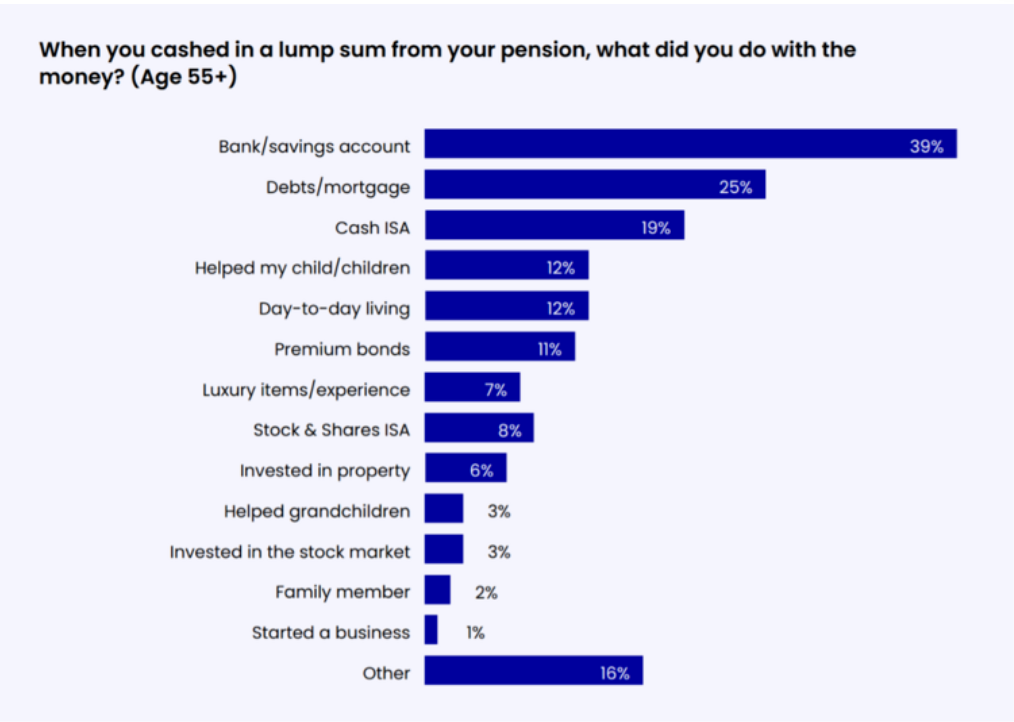

How is the money being used?

Findings from interactive investor’s Great British Retirement Survey 2023, which surveyed 9,000 pension savers, provide insights into how the withdrawn funds are being used.

In response to a multiple-choice question about how they spent their pension withdrawals:

- The largest proportion (39%) placed the money in a bank or savings account

- 19% invested in a cash ISA, and 11% bought Premium Bonds

- One in four (25%) used some or all the money to repay debts and/or a mortgage

- 12% used the cash for day-to-day living expenses

- 12% provided financial assistance to their children.

Source: interactive investor Great British Retirement Survey 2023.

Confidence in pension freedoms

A recent snap poll* of 1,011 visitors to the interactive investor website found overwhelming support for pension freedoms, with 78% preferring the current system over a return to annuities and restricted access.

Regarding confidence in their pension savings:

- 55% felt confident their pension would last

- 32% were somewhat confident

- 13% were not confident.

Myron Jobson, Senior Personal Finance Analyst, interactive investor, says: “Pension freedoms have fundamentally reshaped the retirement landscape, giving savers unprecedented control over how they access and use their hard-earned nest eggs. For many, this flexibility has been a game changer, allowing them to tailor their retirement income to their own needs and aspirations rather than being tied to rigid annuity structures.

“The pension tax-free lump sum is one of the best-loved and most well-understood parts of the post-freedoms pension system. The ability to withdraw a quarter of a pension pot tax-free is hugely beneficial for meeting immediate financial obligations, such as paying off a mortgage, clearing debts, or helping children on to the property ladder.

“Taking a tax-free lump sum or a regular income from your pension is a major financial decision that must be carefully considered. Once withdrawn, the money loses its protection from capital gains tax, dividend tax, and inheritance tax (until April 2027), which could result in a larger tax bill down the line.

“It’s also important to remember that many current retirees still benefit from defined benefit (DB) pensions, which provide a guaranteed income for life. However, these schemes have largely disappeared due to the high costs for employers, meaning future retirees will need to be even more mindful of their pension drawdown strategies.

“With greater freedom comes greater personal responsibility. Without careful planning, there is a real risk of exhausting pension savings too soon, leaving retirees financially vulnerable in later life. The challenge is ensuring that funds not only support a comfortable retirement but also cover unexpected expenses, including potential long-term care costs. Striking a balance between enjoying pension savings today and safeguarding financial security for the future is crucial.”

*Snap poll conducted 26 to 27 March 2025.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.