Why bonds will be back in favour in 2023

7th February 2023 08:51

Government bond yields are at their most attractive levels for years and now have ample scope to move lower given the significant economic fragilities that have built up following the end of the Global Financial Crisis.

Global financial markets are contending with the most aggressive tightening in policy rates in living memory, with highly elevated inflation and central bank balance sheet unwinding also threatening bond valuations. Picking the peak in yields feels like a fool’s errand when faced with such volatility.

However, from a longer-term valuation perspective, the asset class certainly appears cheap. Government bond yields are at their most attractive levels for years and now have ample scope to move lower given the significant economic fragilities that have built up following the end of the Global Financial Crisis. A notable side-effect of central bank balance sheets ballooning after this time was investors increasingly moving into riskier and riskier asset classes.

Unprecedented monetary tightening

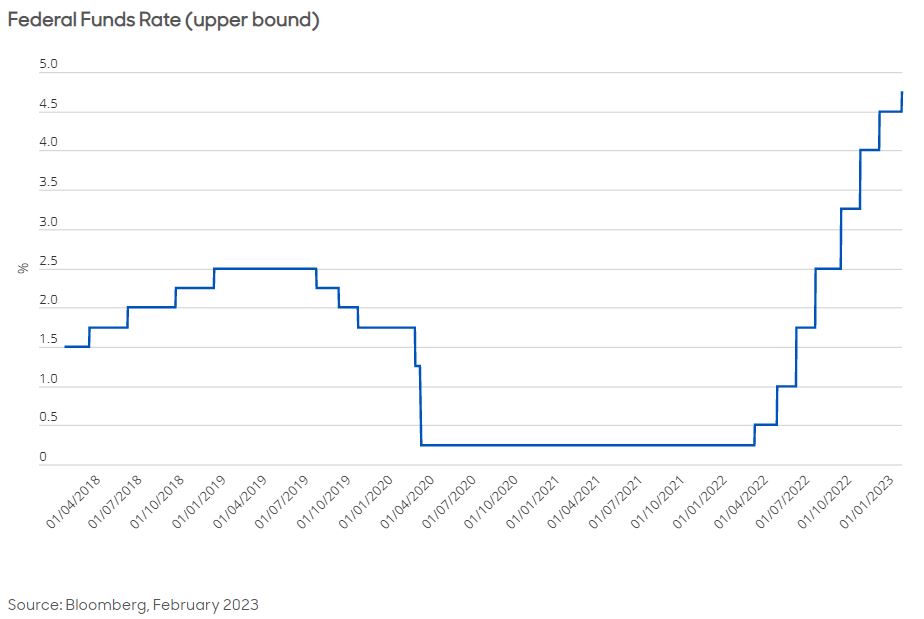

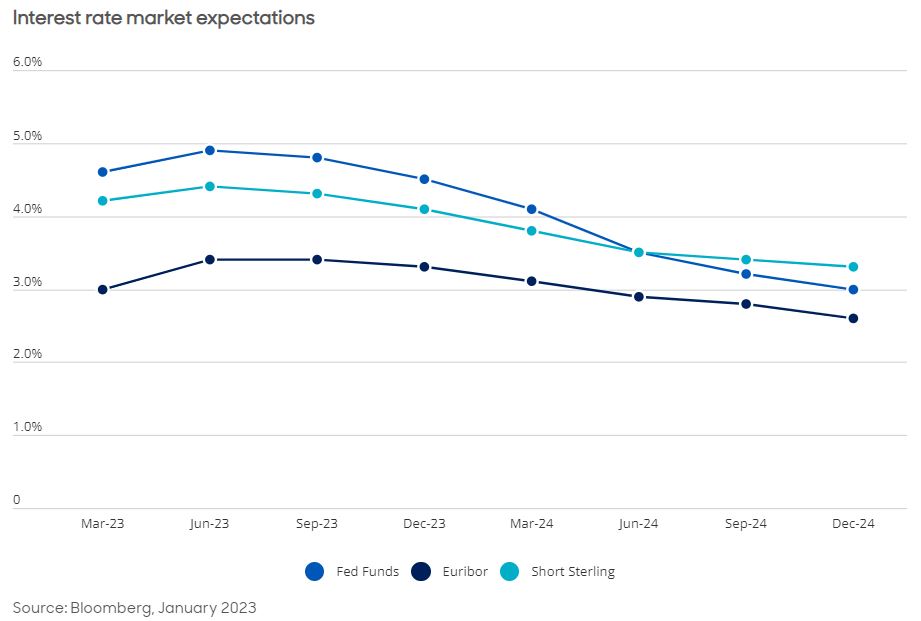

We believe this fragility will resurface in dramatic fashion over coming quarters. Taking the US as an example, the Federal Reserve began tightening in March last year, increasing the Federal Funds Rate (FFR) from a record low of 0.25% to a target range of 4.5-4.75% on 1 February. Current market expectations suggest the FFR will rise to around 5% by May.

For some perspective, during the last hiking cycle, the Fed increased the FFR by 2.25% over a period of three years. So this is an unprecedented speed of monetary tightening, particularly so for a global financial system that had become accustomed to a sustained period of highly accommodative conditions. As such, while this clearly entails risks to the global economy, we believe it could also present some potentially compelling bond investment opportunities in 2023.

Duration view depends on the yield outlook

Duration positioning (or interest rate exposure) necessarily depends on the outlook for yields. We feel it's definitely time to add some duration to portfolios as we believe we have already seen the peak in yields, and the broad trend in yields over the course of 2023 will likely remain downwards.

At the same time, however, we acknowledge that bond yields have already reduced quite significantly from the highs of October last year. Over the short term, elevated inflation, exploding supply and weak sentiment are also major hurdles for sustained bond market outperformance. That’s why we’re more cautious about building too large a position at present.

There's also significant uncertainty in the near term regarding central bank activity, both in the US and globally. Furthermore, we have the additional threat of quantitative tightening, which could be highly disruptive if private investors can’t step up to offset declining central bank participation in government bond markets.

Slowing growth outlook supportive for government bonds

The pickup in global government bond supply from many sources this year could be sizeable if current forecasts are taken at face value, necessitating a greater risk premium from investors. However, we believe that the rise in interest rates and yields globally is already inflicting significant damage on growth, and this will ultimately lead to a mild recession across developed markets.

As economic growth collapses, we should see increasing demand for government bonds as investors rush to 'safe havens' for protection, followed by rising demand also for shorter maturity government bonds when central banks signal they’re pausing their rate-hiking cycle. Given the expected path of policy interest rates, we anticipate our appetite for global government bonds and duration will increase steadily in 2023.

Improved conditions for riskier assets later in the year

The inverse relationship between risk markets and government bonds has been badly damaged, but it is not permanently broken and we believe it will re-assert itself this year. We think higher yields and less central bank intervention will ensure that more normal market conditions should prevail over time. In this regard, we would expect slower economic growth and lower inflation to be positive for government bonds but not so for riskier assets.

However, attractive opportunities for riskier assets should also emerge as the year progresses. Credit spreads are already currently wide of historic averages, suggesting a long-term opportunity. But valuations could improve further as the slowdown leads to weakness in the riskier parts of the bond universe, such as High Yield and emerging markets, as well as wider spreads in Investment Grade bonds.

Ultimately, we believe the data will continue to indicate a contracting economy, which has yet to be fully reflected in earnings expectations and by extension equity and credit valuations. We expect credit spreads to widen at some stage in the coming months, equity prices to drop, and government bonds to rally as the positive correlation between risk assets and interest-rate risk seen in recent years reverts to its more historically typical negative correlation.

Having said that, we don't expect the coming downturns/recessions to be especially deep, and therefore we also anticipate good opportunities to selectively add exposure to riskier bonds too, probably in the second half of the year.

Putting everything together

In summary, albeit with different pathways, our view is that 2023 as a whole will likely be a much better period for most parts of the bond universe – by the end of the year, we anticipate that both Investment Grade and High Yield markets, as well as global government bond markets, should all deliver positive total returns.

Roger Webb, Deputy Head of Sterling Investment Grade at abrdn and Liam O'Donnell, Head of Nominal Rates Management at abrdn

ii is an abrdn business.

abrdn is a global investment company that helps customers plan, save and invest for their future.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.